SALT Deduction Cap Increase: $40K Limit and PTE Workarounds

Gary Gal

The State and Local Tax (SALT) deduction cap has been one of the most debated parts of U.S. tax law since 2017. Originally set at $10,000 under the Tax Cuts and Jobs Act (TCJA), it limited how much state and local tax you could deduct on your federal return. For people in high-tax states like California, New York, and New Jersey, that cap hurts.

Now, starting in 2025, the new One Big Beautiful Bill Act (OBBBA) raises that limit to $40,000, giving millions of taxpayers much-needed relief. But with new rules also come new questions. How does this higher cap work? Does it change the value of pass-through entity (PTE) workarounds? And who really benefits from this shift?

In this guide, we’ll explain everything you need to know about the $40,000 SALT deduction limit, how PTE workarounds still play a role, and how small business owners and professionals can make the most of these changes.

What Is the SALT Deduction Cap (and Why It Matters)

The SALT deduction lets you subtract state and local taxes—such as income, property, or sales taxes—from your federal taxable income. Before 2018, there was no hard limit on this deduction. High earners in states with steep income or property taxes could claim tens of thousands in deductions.

That changed with the Tax Cuts and Jobs Act (TCJA) in 2017. The new rule capped total SALT deductions at $10,000 ($5,000 for married filing separately). This limit hit taxpayers hardest in states with high property taxes and high income taxes.

For small business owners and professionals, the cap often meant losing out on thousands in deductible expenses. Many shifted focus to finding legal workarounds, such as electing a Pass-Through Entity Tax (PTET) at the state level.

The good news is that 2025 brings new flexibility with a higher cap and new planning opportunities.

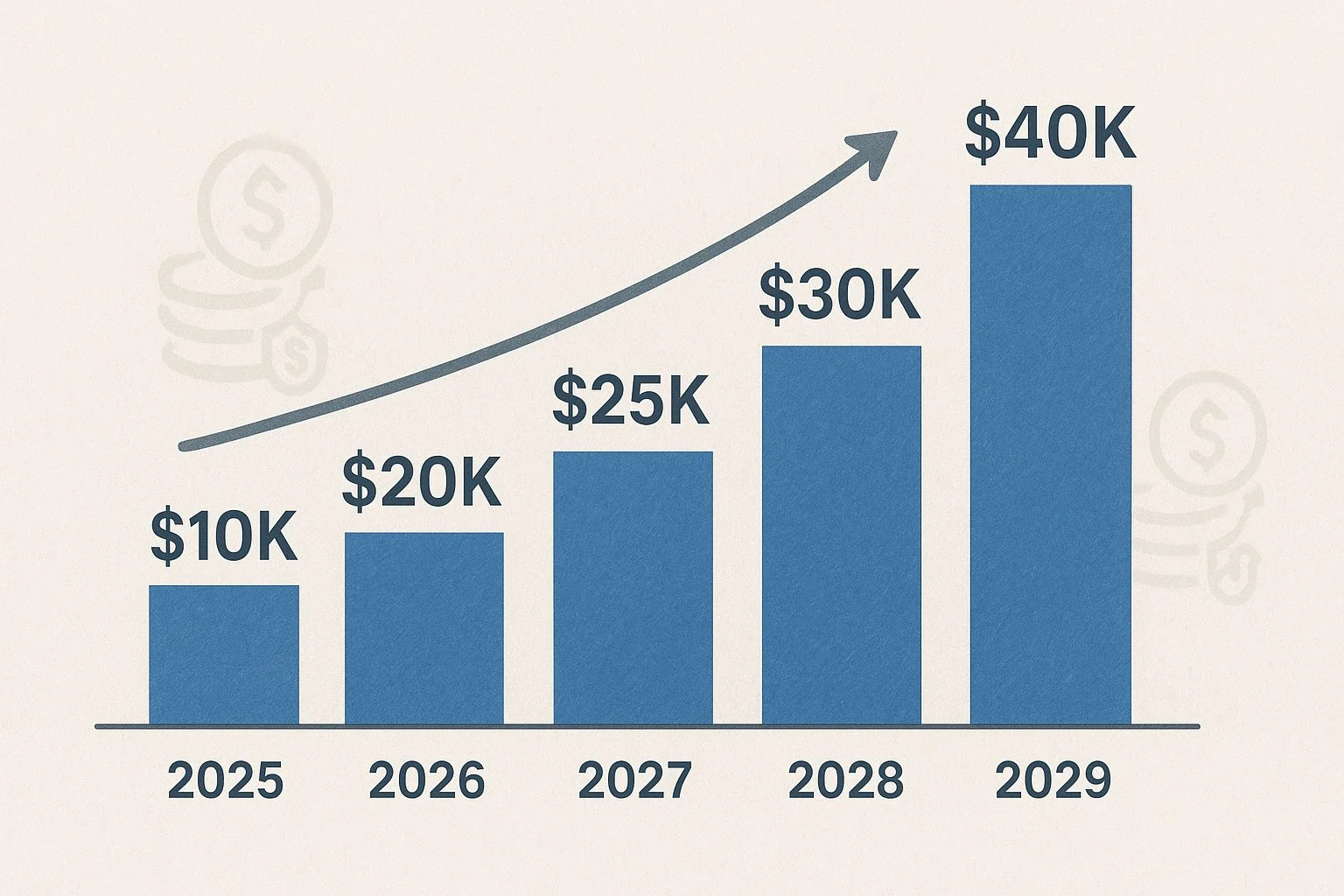

The 2025–2029 SALT Cap Increase Explained

Starting in tax year 2025, the SALT deduction limit rises to $40,000 for most taxpayers. Married couples filing separately can deduct up to $20,000.

This increase will stay in effect through 2029, with the original $10,000 limit returning in 2030 unless Congress extends it. The law also includes a 1% annual inflation adjustment, so the actual cap will rise slightly each year.

Here are the key details:

Effective years: 2025–2029

Limit amount: $40,000 (single/joint) or $20,000 (married filing separately)

Inflation index: 1% annual increase

Income phaseout: Begins at $500,000 Modified Adjusted Gross Income (MAGI), fully phased out at $600,000

Deduction cap for top earners: Beginning in 2026, the value of itemized deductions (including SALT) is limited to 35% for those in the 37% tax bracket

This expanded cap reopens the door for many taxpayers to itemize deductions instead of taking the standard deduction. For example, if you pay $28,000 in combined state and local taxes, you can now deduct the full amount instead of being limited to $10,000.

For high-income taxpayers, however, the phaseout rules may limit the benefit. Anyone earning above $600,000 MAGI effectively reverts to the old $10,000 limit.

Who Benefits Most From the $40K SALT Cap?

The biggest winners are residents of high-tax states and those with substantial property tax bills. If you’re a small business owner, corporate executive, or independent professional in states like California, New York, New Jersey, or Massachusetts, you’re most likely to benefit.

Let’s look at a quick example:

Scenario | SALT Paid | Old Cap | New Cap | Deductible Amount | Tax Savings (Est.) |

Homeowner in CA | $25,000 | $10,000 | $25,000 | +$15,000 | ~$5,000 |

Small business owner in NY | $35,000 | $10,000 | $35,000 | +$25,000 | ~$8,000 |

For many, this change makes itemizing worthwhile again, especially if you combine it with other deductible expenses like mortgage interest or charitable contributions.

However, the new cap doesn’t benefit everyone equally. If you live in a low-tax state or your total SALT burden is under $10,000, you’ll see no real difference. Similarly, high earners above the phaseout range may still hit the old limit.

What Is the PTE Workaround (and How It Works)

The Pass-Through Entity Tax (PTET) workaround became one of the most effective tools for business owners after the SALT cap was introduced in 2017. Here’s how it works:

Normally, state income taxes flow through to business owners’ personal returns, where they’re capped under the SALT limit. But with PTET, the business itself pays the state tax instead of the owner. Because the business pays at the entity level, that tax becomes a deductible business expense for federal tax purposes—bypassing the individual SALT cap.

This structure benefits owners of:

S Corporations

Partnerships

Multi-member LLCs are taxed as partnerships

As of late 2025, over 30 states have adopted PTET laws, including California, New York, Illinois, New Jersey, and Connecticut. Each state’s version is different; some are elective, others automatic, but all aim to restore the full federal deductibility of state income taxes for pass-through entities.

The IRS officially recognizes entity-level deductions for PTET, meaning this workaround remains legitimate and powerful.

Does the $40K Cap Make the PTE Workaround Obsolete?

Not at all. The higher SALT deduction limit helps individuals, but PTE workarounds still matter, especially for business owners.

Here’s why:

The $40K cap is still a cap. Even with the increase, large pass-through entities can owe far more in state tax than $40,000. PTET elections can deduct that full amount at the entity level.

Non-itemizers still benefit. If you take the standard deduction, your personal SALT cap doesn’t matter, but your business can still use the PTET deduction.

It can reduce self-employment taxes. Some PTET structures indirectly lower exposure to federal self-employment tax, depending on state rules.

Income phaseouts don’t affect PTET deductions. Unlike the personal SALT deduction, PTET benefits aren’t phased out at high income levels.

That said, the interplay between the $40K personal cap and PTET rules creates new decisions. Some taxpayers may find the personal deduction sufficient and skip the PTET election to avoid complexity. Others, especially multi-partner businesses, will still find PTET elections highly valuable.

Bottom line: PTET remains relevant, but the optimal choice depends on your income, state, and business structure.

Strategic Planning: Combining the SALT Cap and PTE Workarounds

With both tools available, the smartest move is often to use them together.

Here’s how a combined strategy can work:

Your pass-through entity elects to pay state income tax at the entity level, fully deducting that payment on the business’s federal return.

You, as the owner, also claim personal deductions for property taxes and local taxes—up to the new $40,000 limit.

This “dual deduction” strategy lets you maximize federal savings from both entity-level and personal-level deductions.

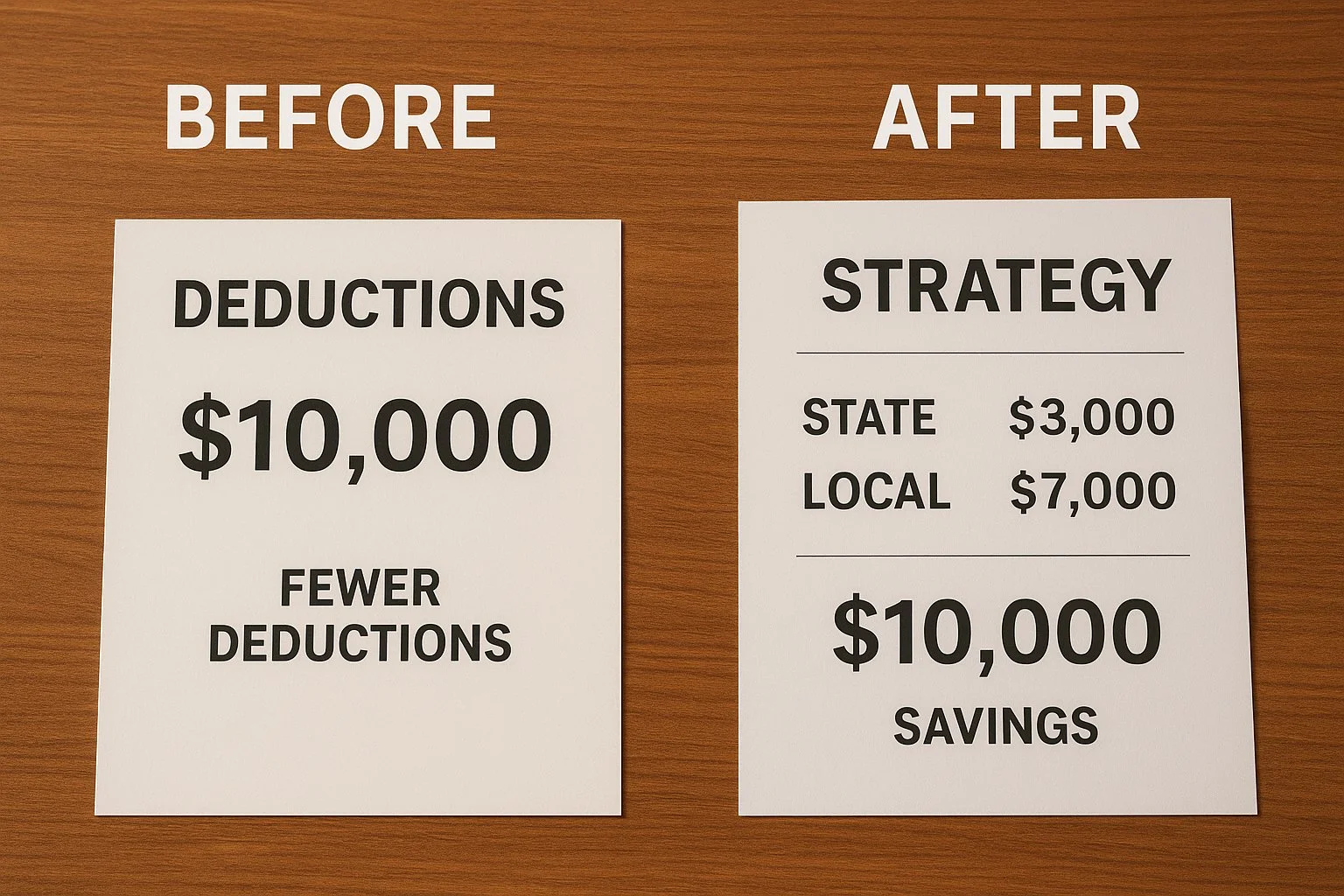

Example:

A small business owner in New York pays $35,000 in state income tax through their S corporation (via PTET) and $15,000 in property taxes personally.

The $35,000 is fully deductible by the entity.

The $15,000 falls under the new $40,000 personal SALT cap.

Total state tax effectively deducted: $50,000.

That’s significantly higher than the old $10,000 limit, which would have capped the total combined deduction.

Planning tips:

Check your state’s PTET election deadline—many require elections early in the tax year.

Coordinate entity payments with your CPA to ensure they’re properly deducted.

Track how PTET credits apply on your state return (some are refundable, others offset state tax).

This hybrid approach can lead to substantial tax savings when structured correctly.

Key Risks and Limitations

Even with these improvements, there are still some important caveats.

1. The change is temporary.

The $40,000 SALT cap only applies from 2025 through 2029. Without congressional action, it will revert to $10,000 in 2030.

2. High-income phaseouts reduce benefits.

Taxpayers above $500,000 MAGI start losing the benefit, and those at $600,000 or above get no increase at all.

3. PTET compliance is complex.

Each state has unique filing deadlines, payment requirements, and credit systems. Errors can lead to lost deductions or double taxation.

4. Federal limits may tighten later.

Future tax reforms could restrict PTET benefits, especially if lawmakers aim to offset revenue losses.

5. Multi-state businesses face added complexity.

If your business operates in more than one state, PTET rules may overlap or conflict. You may need to track apportionment carefully.

Being proactive with a qualified CPA or tax attorney is the best way to ensure you get the intended benefit without creating compliance issues.

Action Steps for Small Business Owners and Professionals

Here’s how to prepare for the 2025 SALT deduction changes:

1. Review your 2024 tax data.

Estimate your 2025 income and potential SALT obligations. Determine if itemizing now beats taking the standard deduction.

2. Check your eligibility for PTET.

Find out whether your state allows a PTET election, when it must be made, and how credits flow back to you as an owner.

3. Coordinate with your CPA early.

Many PTET elections must be made early in the tax year—often by the first or second estimated payment date.

4. Keep detailed records.

Maintain documentation for both entity-level payments and personal tax deductions to ensure clean audit trails.

5. Plan ahead for 2030.

Unless Congress acts, this window closes in five years. Build long-term strategies that can adapt if the cap drops again.

Conclusion

The SALT deduction cap increase offers meaningful relief to individuals and small business owners who have been limited by the $10,000 ceiling since 2017. By raising the limit to $40,000, Congress has restored some fairness for taxpayers in high-cost, high-tax regions.

Still, this is not a one-size-fits-all solution. The PTE workaround continues to offer valuable savings opportunities for pass-through business owners. When used together, the two strategies can unlock significant tax deductions—especially for those who plan and coordinate with professionals.

The key takeaway: The next few years (2025–2029) present a rare opportunity to maximize both personal and business deductions before the rules change again. If you run a business or manage significant state taxes, now’s the time to review your strategy, elect PTET if available, and capture every deduction you’re entitled to.

Note: If you are a small business owner looking to lower taxes further, our comprehensive guide on Maximizing PTE Deductions walks through practical strategies and year-end planning tips to make the most of your PTE election.

Frequently Asked Questions

What is the new SALT deduction limit for 2025?

For tax year 2025, the SALT deduction cap has increased from $10,000 to $40,000 for individuals (and $20,000 for married filing separately). This limit applies to combined state and local income, sales, and property taxes.

How long will the $40,000 SALT deduction cap last?

The higher SALT deduction cap applies from 2025 through 2029. Unless Congress extends it, the cap will revert to $10,000 starting in 2030.

Who qualifies for the SALT cap increase?

Taxpayers who itemize deductions and have state and local tax payments above $10,000 may qualify. However, those with MAGI over $500,000 will see a phaseout, and the benefit fully disappears at $600,000 MAGI.

How does the $40,000 SALT deduction work for married couples?

Married couples filing jointly can claim the full $40,000 deduction. Those filing separately are limited to $20,000 each. The deduction applies to combined income, property, and sales taxes.

What is the PTE workaround for the SALT cap?

The Pass-Through Entity Tax (PTET) workaround lets partnerships, S corporations, and certain LLCs pay state taxes at the entity level instead of the personal level. This allows business owners to bypass the SALT cap on their individual returns.

Do PTE workarounds still matter with the higher $40,000 cap?

Yes. Even with the higher cap, PTE elections can offer additional tax benefits, especially for owners of profitable businesses. They can still deduct state taxes at the entity level and potentially reduce self-employment taxes.

Which states allow a PTE tax election?

As of 2025, over 30 states have adopted a pass-through entity tax (PTET) option, including California, New York, Illinois, Texas, New Jersey, and Massachusetts. Each state has unique rules, election deadlines, and credit structures.

Can I deduct more than $40,000 in state and local taxes under the new rules?

Not personally. The $40,000 cap is the maximum deduction for individuals on their federal return. However, business owners using PTET elections may still deduct more at the entity level.

How do income phaseouts affect the SALT deduction?

If your Modified Adjusted Gross Income (MAGI) exceeds $500,000, your SALT deduction begins to phase out. Once income reaches $600,000, you revert to the original $10,000 limit, effectively losing the increased benefit.

Should I itemize or take the standard deduction in 2025?

If your total itemized deductions, including SALT, mortgage interest, and charitable contributions, exceed the standard deduction, itemizing is worth it. The new $40,000 cap means more taxpayers in high-tax states may find itemizing beneficial again.