Income Tracking for Small Businesses in Great Neck Estates, NY

Gary Gal

I have worked with small businesses in Great Neck Estates, NY, and I often see owners struggle to keep accurate income records. At Andemax, we’ve helped clients fix inconsistent tracking systems that quietly distort financial decisions.

Effective income tracking for small businesses in Great Neck Estates, NY, requires consistent recording of all revenue, clear categorization, and regular reconciliation with bank data. This means using reliable tools and disciplined processes to maintain accurate financial visibility.

If your numbers feel unclear, the issue is rarely effort; it is usually structure. The rest of this article breaks down practical ways to tighten your system and avoid costly blind spots.

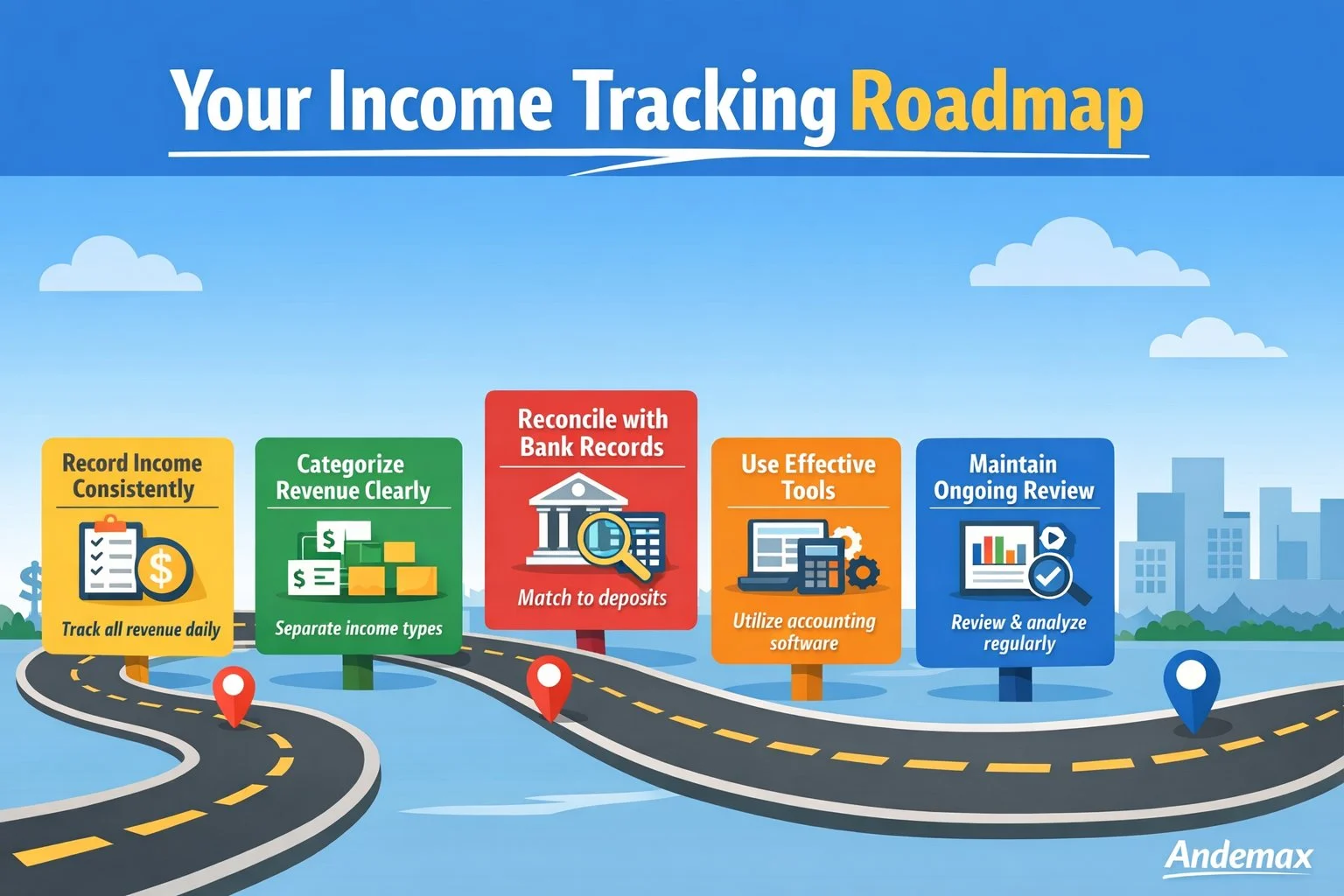

Key Takeaways

Record Income Consistently: Track all revenue daily with standardized entries to prevent costly errors.

Categorize Revenue Clearly: Separate product, service, recurring, and one-time income for accurate insights and better decisions.

Reconcile with Bank Records: Match income to deposits regularly to catch discrepancies and maintain reliable financial data.

Use Effective Tools: Accounting software with integrations reduces errors, saves time, and scales with your business.

Maintain Ongoing Review: Monitor records regularly and analyze trends to ensure long-term accuracy and control.

Next, we’ll dive into the main sections of the blog to explain how to strengthen income tracking and financial control.

Keep Your Income Records Accurate and Reliable. [Schedule Your Income Tracking Review Here] or call our Great Neck Estates office at (800) 344-5226 for expert guidance.

Establish a Consistent Process for Recording Income

A consistent process for recording income is a standardized method for capturing all business revenue accurately and in a timely manner. It works by applying uniform data entry practices, structured documentation, and regular updates to ensure financial records remain complete and reliable.

The key steps and components of this process are outlined in the structured list that follows.

Record income daily

Log every sale or payment at the end of each day

Use a notebook, spreadsheet, or software

Standardize your entries

Include date, amount, source, and payment method

Keep naming consistent to avoid confusion later

Store proof of transactions

Save receipts, invoices, and screenshots

Organize them by date or category

Review weekly

Check for missing entries

Confirm totals match expectations

To ensure all income is properly documented and compliant, explore this in-depth guide on the essential financial records for businesses in Great Neck Estates, NY.

Categorize Revenue Streams Clearly and Accurately

Categorizing revenue streams clearly and accurately involves classifying all sources of business income into distinct, meaningful groups for analysis and reporting. A common challenge lies in inconsistent or overlapping categories, which can distort financial insights and reduce the reliability of performance evaluations.

The subtopics below address the key distinctions and considerations required to structure revenue categories effectively.

Product vs Service Revenue

Product revenue refers to income generated from the sale of tangible goods, while service revenue comes from delivering expertise, labor, or time-based work. This distinction is essential because each type involves different cost structures, pricing models, and scalability factors that impact profitability analysis.

The key characteristics and examples of each revenue type are outlined in the comparison below:

Product Revenue

Income from the sale of physical or digital goods

Typically involves inventory or stock management

Usually, one-time transactions per sale

Cost structure includes production, storage, and distribution

Example: Retail items, packaged products

Service Revenue

Income from providing skills, expertise, or labor

Often time-based or project-based

May involve customized or client-specific work

Cost structure is driven mainly by time and labor

Example: Consulting, repairs, design services

Make sure to track your product and service income separately.

Recurring vs One-Time Income

Recurring income consists of payments that occur on a regular, predictable schedule, while one-time income arises from singular or irregular transactions. Understanding this distinction is critical because recurring revenue provides stability and forecasting accuracy, whereas one-time payments are less predictable and require separate monitoring.

The table below presents the key differences between these income types, highlighting their characteristics and examples:

Income Type | Description | Example |

Recurring Income | Repeats regularly | Subscriptions, retainers |

One-Time Income | Happens once or irregularly | Project-based work |

Focus on growing recurring income because it stabilizes your business. One-time income can boost revenue, but it should not be your foundation.

Local vs Online Sales

Local sales refer to revenue generated through in-person or geographically nearby transactions, while online sales come from digital platforms and remote channels. Consequently, separating these categories improves visibility into customer behavior, cost structures, and channel-specific performance differences.

The list below outlines the defining characteristics and typical sources associated with each sales channel.

Here’s how to categorize:

Local Sales

In-person transactions at a physical location

Payments collected via cash or local bank transfer

Revenue tied to a specific geographic area

Examples include walk-in customers and local deliveries

Online Sales

Transactions completed through digital platforms

Payments processed via gateways, e-wallets, or cards

Revenue generated beyond local geographic limits

Examples include e-commerce stores, social media sales, and digital services

Track local and online sales separately in your accounting system to identify growth opportunities and optimize marketing strategies for each channel.

Once income is recorded and categorized, the next step is understanding how it performs after costs are applied at the project level. That is where job costing for contractors becomes essential, revealing true profitability across each job.

Reconcile Income with Bank and Payment Records Regularly

Reconciling income with bank and payment records regularly is the process of systematically comparing recorded transactions against actual deposits to ensure accuracy. Errors, timing differences, and missing entries are common challenges that can distort financial reporting and hinder reliable decision-making.

The subsequent subtopics provide a structured approach to matching deposits, resolving discrepancies, and establishing an effective reconciliation schedule.

Matching Deposits with Recorded Income

Matching deposits with recorded income involves verifying that every transaction logged in the accounting records corresponds exactly to an actual deposit in a bank or payment accounts. This step is essential because unmatched entries can indicate errors, missing payments, or timing discrepancies that compromise the integrity of financial data.

Follow the key steps below to systematically perform this matching process for reliable and accurate records:

Gather Records

Collect all income entries from accounting software or ledgers

Include invoices, receipts, and payment confirmations

Compare with Bank Statements

Review each deposit listed in the bank or payment accounts

Match them to the corresponding recorded transactions

Identify Discrepancies

Flag any deposits without matching entries

Note any recorded income not reflected in bank statements

Resolve Issues

Investigate missing or extra transactions

Adjust records or follow up with payment sources as needed

Confirm Accuracy

Ensure totals align between records and bank statements

Document reconciliation for auditing and future reference

Common issues include duplicate entries, forgotten sales, or timing differences. Fix them immediately before they compound.

Handling Discrepancies

Handling discrepancies involves identifying and correcting differences between recorded income and actual deposits to maintain accurate financial records. These differences can arise from errors, timing delays, or misclassified transactions, and resolving them promptly prevents compounding mistakes and ensures reliable reporting.

The list below details common causes of discrepancies along with recommended actions to address each effectively:

Missing income

Check whether the payment was recorded but not deposited

Verify invoices, receipts, and customer confirmations

Extra deposits

Determine if the deposit belongs to another transaction or account

Reclassify or correct the entry as needed

Incorrect amounts

Compare recorded income with actual payment amounts

Adjust records to reflect the accurate value

Create a habit of resolving issues the same day you find them. Delay only increases confusion.

Setting a Reconciliation Schedule

A reconciliation schedule should be established based on the volume and frequency of business transactions to maintain accurate financial records. Regularly scheduled reconciliations prevent errors from accumulating and ensure that discrepancies are identified and resolved promptly.

The table below outlines recommended reconciliation frequencies for different business sizes and transaction volumes:

Business Type | Recommended Frequency | Reasoning |

High-Volume Small Business | Daily | Frequent transactions require immediate checks to prevent errors from accumulating |

Average-Volume Small Business | Weekly | Weekly review balances workload with timely detection of discrepancies |

Low-Volume Small Business | Monthly | Limited transactions reduce the risk of errors, making monthly reconciliation sufficient |

Choose one and stick to it. Consistency matters more than frequency.

Choose the Right Tools for Reliable Tracking

Selecting the right tools for reliable tracking involves implementing systems or software that consistently capture, organize, and report all income data. One frequent obstacle is ensuring these tools integrate smoothly with existing workflows and financial accounts to prevent errors or duplicated entries.

The sections that follow explore system types, software options, and integration strategies that enhance accuracy and efficiency in income tracking.

Manual vs Digital Systems

Manual systems rely on paper or spreadsheets to record income, while digital systems use software to automate and streamline financial tracking. Digital solutions reduce human error and improve scalability, whereas manual methods can become cumbersome as transaction volume grows.

The table below compares key features, benefits, and limitations of both approaches for clear evaluation:

Feature | Manual System | Digital System |

Ease of Use | Simple to start, minimal setup | Requires initial setup, may need training |

Accuracy | Prone to human error | High accuracy with automated calculations |

Scalability | Limited as transactions grow | Easily handles increasing volume |

Time Efficiency | Time-consuming | Faster data entry and reporting |

Cost | Low upfront cost | May involve subscription or software fees |

If your business is growing, manual tracking will eventually fail you.

Accounting Software Options

Accounting software options consist of digital tools designed to record, categorize, and report all business income efficiently. Their value lies in features such as easy income entry and categorization, automated bank syncing, clear reporting dashboards, and cost-effective pricing, which together streamline financial management.

The list below highlights these key capabilities and explains how each contributes to accurate and efficient income tracking:

Easy Income Entry and Categorization

Allows transactions to be logged quickly and organized by type, reducing manual errors.Automated Bank Syncing

Automatically imports bank and payment data to keep records current and accurate.Clear Reporting Dashboards

Provides visual summaries of income, trends, and key metrics for informed decision-making.Affordable Pricing

Ensures small businesses can access robust financial tools without high costs.

Test before committing. A tool that looks good but feels confusing will not last.

Integration with Banks and Payment Platforms

Integration with banks and payment platforms ensures that all transactions are automatically recorded and synchronized with the accounting system. This connection reduces manual entry errors, saves time, and provides a real-time view of cash flow across multiple channels.

The list below highlights key integrations, their functions, and the benefits they provide for accurate income tracking:

Bank Account Integration

Automatically imports deposits and withdrawals

Reduces manual entry errors

Provides up-to-date account balances

Payment Gateway Integration

Syncs transactions from platforms like PayPal, Stripe, or Square

Ensures all digital payments are recorded accurately

Facilitates faster reconciliation

E-commerce Platform Integration

Connects online stores to accounting software

Automatically tracks sales, refunds, and fees

Supports multi-channel revenue visibility

Mobile Payment Integration

Captures payments from mobile wallets and apps

Maintains consistent transaction records

Enhances accessibility for small business operations

If not, expect more manual work and a higher risk of errors.

Maintain Ongoing Review and Financial Discipline

Maintaining ongoing review and financial discipline involves continuously monitoring income records and enforcing consistent accounting practices. This approach ensures that errors are detected early, trends are analyzed accurately, and financial decisions are based on reliable data.

The list below outlines key review practices and disciplined habits that support long-term accuracy and control in income tracking:

Monthly Financial Reviews

Examine income statements and bank reconciliations

Identify trends, discrepancies, and anomalies

Adjust records or categories as needed

Trend Analysis

Compare revenue across months or years

Detect seasonal fluctuations or growth opportunities

Inform budgeting and forecasting decisions

Process Audits

Review adherence to recording and categorization procedures

Ensure reconciliation schedules are followed

Identify gaps or inefficiencies in the system

Consistent Documentation

Keep receipts, invoices, and digital records organized

Standardize naming conventions and data entry

Support accuracy and ease of retrieval

Regular Staff Training

Educate team members on proper recording and reconciliation practices

Reinforce accountability and minimize errors

Promote a culture of financial discipline

You do not need perfection. You need consistency and awareness.

Prevent revenue blind spots before they hurt your business. [Schedule Your Free Income Review Here] or call (800) 344-5226 today to strengthen your financial tracking

How an Accounting Firm Strengthens Income Tracking and Financial Control

An accounting firm strengthens income tracking and financial control by establishing reliable systems and enforcing accurate financial practices. Moreover, this support ensures that income data is consistently recorded, verified, and aligned with compliance requirements.

The key services and functions that support these outcomes are outlined in the list below:

System Setup and Process Design – Standardize income workflows, define revenue categories, and ensure consistent records.

Software Selection and Implementation – Recommend and configure tools, integrating them with banks and payment platforms.

Bank and Payment Reconciliation – Match deposits, resolve discrepancies, and maintain audit-ready records.

Financial Reporting and Analysis – Generate reports, track trends, and support informed decisions.

Compliance and Risk Management – Ensure accurate tax reporting and reduce audit exposure.

Ongoing Advisory and Oversight – Monitor processes, recommend improvements, and guide financial controls.

Explore the full range of professional solutions available by visiting us at Andemax.

Summary Table

Component | Key Action | Benefit |

Recording Process | Track income daily | Prevent missing data |

Categorization | Separate revenue types | Better insights |

Reconciliation | Match records with the bank | Accurate financial data |

Tools | Use reliable software | Efficiency and scalability |

Ongoing Review | Monitor regularly | Long-term financial control |

Conclusion

Income tracking for small businesses in Great Neck Estates, NY, is not just a bookkeeping task; it is the foundation for strategic decision-making and financial stability. Without a disciplined system, even profitable businesses can face cash flow blind spots that erode growth and profitability.

A common mistake experienced accountants see is failing to reconcile digital payments with bank deposits, which silently inflates reported income. Catching this early ensures accurate reporting, prevents audits, and avoids costly misallocations.

The risk of sloppy tracking is financial mismanagement and lost opportunities, while the reward of precise, consistent records is actionable insight and stronger business control. For a confidential review of your system, contact our Great Neck Estates firm at Andemax on (800) 344-5226 to protect your financial future.

Frequently Asked Questions

What is the best way to track income for a small business?

The best way is to record all income consistently using a structured system and reliable tools. Regular reconciliation with bank records ensures accuracy and prevents errors from building up over time.

How often should I update my income records?

You should update your income records daily or at least weekly, depending on transaction volume. Frequent updates reduce errors and make reconciliation faster and easier.

Why is categorizing income important?

Categorizing income helps you understand where your money comes from and which areas perform best. This insight allows you to make better financial and strategic decisions.

Can I track income without accounting software?

Yes, you can use spreadsheets or manual methods, especially when starting. However, as your business grows, digital tools become necessary for accuracy and efficiency.

What happens if I do not reconcile my income records?

Without reconciliation, your records may not match actual bank transactions, leading to inaccurate financial data. This can result in poor decisions and potential financial risks.

How do I handle missing or incorrect income entries?

You should investigate discrepancies immediately by checking receipts, invoices, and bank statements. Fix errors as soon as possible to keep your records accurate and reliable.

Is income tracking necessary for very small businesses?

Yes, even the smallest businesses need proper income tracking to understand performance and manage cash flow. Skipping this step creates confusion and limits growth potential.