Smart Tax-Saving Strategies for 6-Figure Business Owners in New York

Gary Gal

Across years advising six-figure clients, I’ve seen New York business owners overpay taxes due to missed planning opportunities. In our work at Andemax, we help build practical tax-saving strategies for business owners in NY who want clearer, legal ways to reduce costs.

Because of these common gaps, smart approaches focus on entity selection, retirement contributions, expense timing, and credits under New York rules. These methods lower taxable income while staying compliant with state and federal laws.

So, the right mix depends on your income level, industry, and long-term goals. Next, we break down each strategy so you can apply the ones that fit your business.

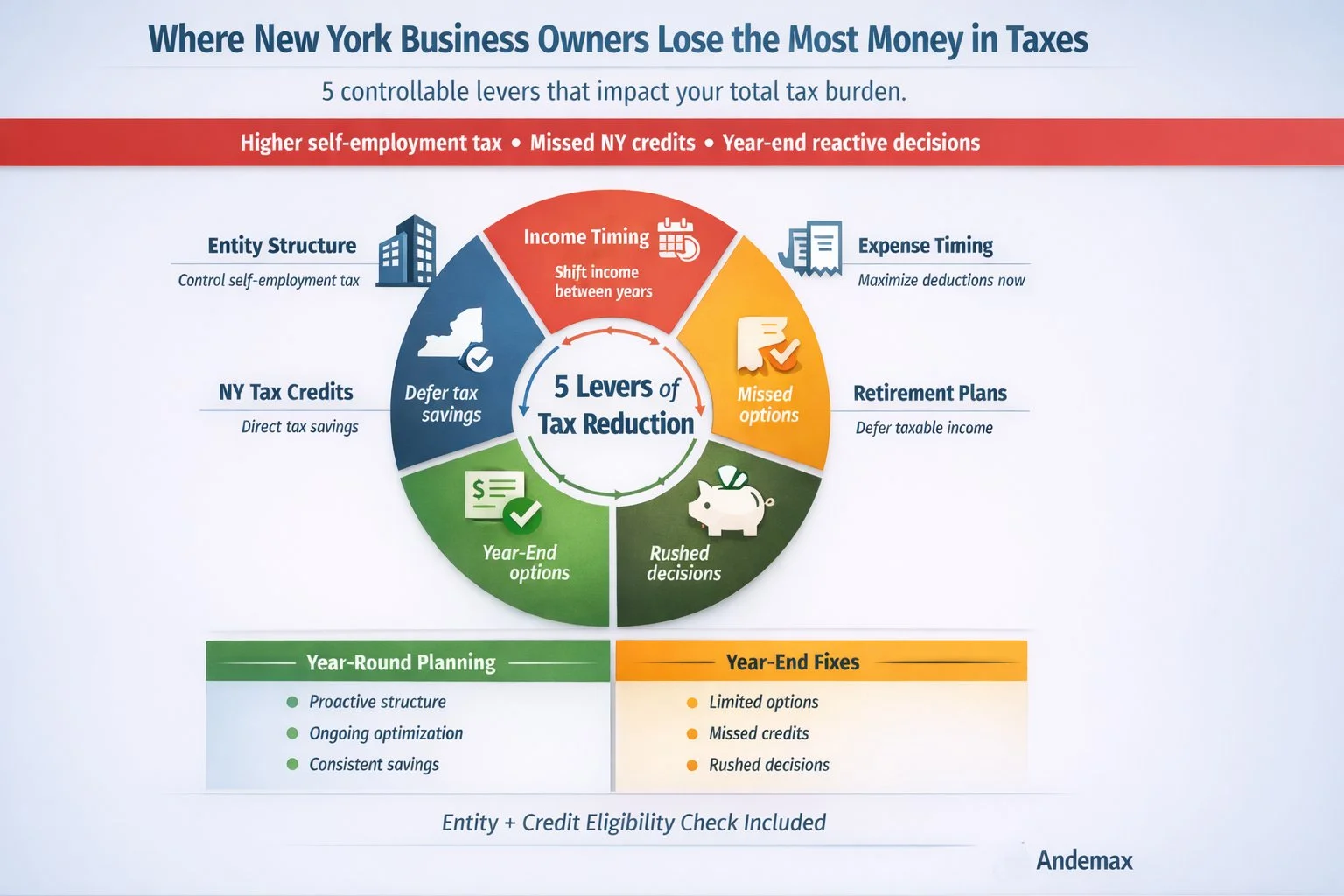

Key Takeaways

Entity choice impacts total tax burden, so selecting the wrong structure can lead to avoidable overpayment.

Retirement contributions and expense planning reduce taxable income, helping prevent missed savings at year's end.

Income and expense timing affect tax brackets, so poor timing can increase overall liability.

New York credits require early planning and records, so missing documentation can cost valuable tax savings.

What Tax-Saving Strategies Should Business Owners in NY Focus on First?

Effective tax-saving strategies for business owners in NY prioritize early planning to legally reduce taxable income and overall liability. This works by aligning entity structure, income timing, deductions, and credits with New York and federal tax rules. Review the key strategies below to identify ways to reduce your tax burden efficiently.

Entity selection aligns tax treatment with income structure, helping reduce overall liability

Retirement contributions defer income while building long-term financial security

Income timing manages when revenue is recognized to control tax bracket exposure

Expense timing accelerates deductions to offset higher income periods

New York tax credits directly reduce taxes owed when eligibility and documentation are met

See what you're missing in your tax strategy! [Schedule a Tax Review Today Here] or call us at (800) 344-5526.

Choosing the Right Business Entity for Lower Taxes

Entity selection determines how a business is taxed at the federal and state levels. Different structures affect income classification, self-employment tax exposure, and compliance complexity.

Explore how each option changes your tax position through the section below.

Sole Proprietorship vs LLC vs S Corporation

Entity choice defines how business income is reported and taxed across different structures. Each option affects liability, self-employment taxes, and administrative complexity differently.

Use the table below to compare options and choose what fits your tax and business needs:

Entity Type | Tax Treatment | Liability | Key Consideration |

Sole Proprietorship | Personal income tax | Unlimited personal liability | Simplest setup but highest exposure |

Pass through taxation (default) | Limited liability protection | Flexible structure with optional tax elections | |

S Corporation | Salary plus distributions | Limited liability protection | Requires payroll, but may reduce self-employment taxes |

Tax Treatment Differences by Entity Type

Tax treatment determines how profits are classified and taxed under each business structure. Variations exist in payroll taxes, pass-through income, and corporate-level obligations.

Review the table below to see how each entity affects your taxable income.

Entity Type | Tax Method | Key Impact |

Sole Proprietorship | Personal income tax | Highest self-employment tax exposure |

LLC | Pass-through taxation | Flexible tax classification options |

S Corporation | Salary plus distributions | Potential payroll tax reduction |

Common Mistakes in Entity Selection

Entity selection errors often lead to unnecessary tax burdens and compliance issues. Many businesses choose structures without considering long-term income growth or payroll implications.

Check the list below and avoid mistakes that could cost your business more in taxes:

Ignoring long-term income projections

Overlooking the self-employment tax impact

Choosing structure without state tax analysis

Using Retirement Contributions to Reduce Taxable Income

Retirement contributions allow business owners to defer income while reducing current taxable earnings. Contribution limits, plan types, and eligibility rules often create confusion in implementation.

Practical options become clear as you move through the sections ahead.

SEP IRA Contribution Rules

SEP IRA rules define how business owners contribute pre-tax income toward retirement savings. Contribution limits depend on compensation percentages and annual IRS thresholds.

Review the key rules below to understand how much you can contribute:

Contribution limit: Up to 25% of compensation

Annual cap: Set by the IRS each year

Employer-funded only: No employee salary deferrals

Solo 401(k) Advantages for Owners

Solo 401(k) plans allow business owners to contribute as both employer and employee. This dual role increases contribution limits and enables faster tax-deferred growth.

Explore the benefits below to see how this plan strengthens your tax strategy:

Employee deferral plus employer contribution

Higher total contribution limits than SEP IRA

Option for Roth contributions

How Contribution Limits Impact Tax Savings

Contribution limits set the maximum amount that can be reduced from taxable income each year. Higher limits create more opportunities to defer income and lower current tax liability.

Check the table below to compare limits and plan your contributions effectively:

Plan Type | Contribution Structure | Tax Saving Potential |

SEP IRA | Employer only | Moderate |

Solo 401(k) | Employee plus employer | Higher |

Timing Income and Expenses for Better Tax Outcomes

Income and expense timing are managed when earnings and deductions appear for tax purposes. Cash flow constraints and IRS rules often limit flexibility in execution.

Getting timing right becomes clearer as you move through the strategies below.

Deferring Income to Lower Tax Brackets

Deferring income shifts revenue recognition to a later tax year to reduce current tax exposure. This works when future income is expected to be lower or when tax rates decrease.

Review the steps below to delay income and manage your tax bracket effectively:

Delay invoicing near year-end

Postpone contract completion when possible

Defer bonus or distribution payments

Negotiate later payment terms with clients

Use cash basis accounting when eligible

Time asset sales for lower-income years

Accelerating Deductible Business Expenses

Accelerating expenses moves deductible costs into the current year to offset higher income. This strategy increases deductions when tax rates or profits are elevated.

Check the list below to bring forward expenses and reduce taxable income now:

Prepay rent or insurance

Purchase needed equipment before year-end

Increase retirement contributions

Stock up on necessary supplies

Pay outstanding vendor invoices early

Invest in business-related software or tools

Year-End Tax Planning Considerations

Year-end planning reviews financial activity to identify last-minute tax-saving opportunities. It involves adjusting income, expenses, and contributions before the tax year closes.

Follow the checklist below to finalize decisions and optimize your tax position:

Review profit and loss statements

Maximize eligible deductions and credits

Confirm retirement contributions and deadlines

Evaluate estimated tax payments

Reconcile all accounts and records

Consult a tax professional for final adjustments

For a more detailed breakdown tailored to pass-through entities, review our Year-End Tax Planning Checklist for PTEs to refine your final decisions.

Leveraging New York-Specific Tax Credits and Deductions

New York tax credits and deductions reduce state tax liability beyond federal adjustments. Eligibility rules and documentation requirements often restrict access for many businesses.

You’ll see how to navigate these benefits more clearly in the sections below.

New York Small Business Credits Overview

New York small business credits reduce state tax liability through targeted incentive programs. These credits apply to hiring, investment, and innovation, with strict eligibility requirements.

Review the table below to compare credits and decide which ones fit your business:

Credit | Who Qualifies | Key Benefit |

Excelsior Jobs Program | Businesses creating new jobs in NY | Tax credits tied to job creation and investment |

Investment Tax Credit | Companies purchasing equipment or property | Reduces the cost of capital investments |

R&D Credit | Businesses conducting qualified research | Offsets innovation-related expenses |

Hire a Veteran Credit | Employers hiring qualified veterans | Direct tax reduction per eligible hire |

Employee Training Incentive | Businesses training employees | Covers workforce development costs |

Industry-Specific State Tax Incentives

Industry-specific incentives provide tax benefits tailored to sectors like manufacturing, tech, and media. Qualification depends on industry type, spending levels, and job creation metrics.

Compare the options below to identify incentives aligned with your operations:

Incentive | Target Industry | Key Benefit |

Manufacturing Investment Credit | Manufacturing | Reduces the costs of production equipment |

Digital Gaming Media Credit | Tech and gaming | Supports game development expenses |

Film Production Credit | Film and media | Covers production and labor costs |

Green Energy Incentives | Renewable energy | Encourages sustainable investments |

Life Sciences Credit | Biotech and research | Offsets R&D and innovation costs |

Documentation Requirements for Claiming Credits

Documentation requirements ensure that claimed credits meet New York State compliance standards. Proper records support eligibility, accuracy, and audit readiness.

Follow the checklist below to organize documents and support your credit claims:

Maintain detailed financial statements and expense records

Keep payroll reports and employee qualification data

Document all eligible investments and related receipts

File required tax forms and credit applications accurately

Store contracts and supporting agreements for verification

Take control of your New York tax strategy and avoid costly overpayments with proactive planning. [Schedule Your Free Tax Strategy Review] or call (800) 344-5226 for expert guidance today.

How an Accounting Firm Can Help Business Owners Maximize Tax Savings in New York?

An accounting firm provides professional tax planning and compliance services that help businesses reduce overall tax liability. This involves analyzing financial data, applying tax regulations, and identifying legal deductions and credits at both the federal and state levels.

The services below show how an accounting firm strengthens your tax position and improves efficiency:

Entity structure optimization

Year-round tax planning

Federal and NY tax credits

Expense and deduction tracking

Record keeping and audit support

Payroll and compensation planning

Year-end tax review

Improve your New York tax strategy and reduce liabilities with our expert accounting services designed for business owners.

Summary of Tax-Saving Strategies for New York Business Owners

Strategy Area | What It Involves | Why It Matters |

Entity Structure | Choosing LLC, S Corp, or other setup | Directly affects self-employment tax and overall liability |

Income & Expense Timing | Controlling when income and deductions occur | Helps avoid higher tax brackets and improves cash flow control |

Retirement Contributions | Using SEP IRA or Solo 401(k) plans | Lowers taxable income while building long-term wealth |

New York Tax Credits | Applying state-specific incentive programs | Reduces taxes owed beyond standard deductions |

Documentation & Compliance | Maintaining records for deductions and credits | Prevents disqualification, penalties, and missed savings |

Conclusion

Strong tax-saving strategies for business owners in NY rely on disciplined structure, timing, and documentation that work together throughout the year. Most overpayments happen when decisions are delayed until year-end instead of being built into ongoing planning.

Experienced practice shows a recurring blind spot where credits and deductions are identified too late to qualify or optimize fully. The downside is unnecessary tax leakage and avoidable compliance risk, while the upside is sustained savings and stronger financial control.

Andemax encourages a confidential review before your next filing cycle locks in those outcomes. Contact our Great Neck Estates firm at (800) 344-5226 to assess your tax position with a focused, professional review.

Frequently Asked Questions

What are the best tax-saving strategies for business owners in NY?

The most effective strategies include entity optimization, retirement contributions, and expense timing. New York business owners also benefit from state tax credits when properly documented and planned.

Does an LLC reduce taxes in New York?

An LLC does not automatically reduce taxes, but it offers flexible tax classification options. Proper structuring can lower self-employment taxes when paired with the right election.

Is an S Corporation better for taxes than an LLC?

An S Corporation can reduce self-employment taxes by splitting salary and distributions. However, it requires payroll compliance and may not benefit lower-income businesses.

What business expenses are tax-deductible in New York?

Common deductible expenses include rent, payroll, equipment, software, and professional services. Expenses must be ordinary, necessary, and properly documented to qualify.

How do retirement plans reduce business taxes?

Retirement plans like SEP IRA and Solo 401(k) reduce taxable income through pre-tax contributions. These contributions defer taxes while supporting long-term savings growth.

What New York tax credits are available for small businesses?

Credits include hiring incentives, investment credits, and R&D benefits depending on eligibility. These directly reduce taxes owed rather than just lowering taxable income.

Do I need an accountant for business taxes in New York?

An accountant helps optimize deductions, credits, and compliance with state and federal rules. Professional guidance reduces errors that often lead to overpayment or audits.