Tax-Saving Strategies for Small Business Owners with an LLC

Gary Gal

Running a small business comes with a lot of benefits, including freedom, flexibility, and the satisfaction of having something you can call your own. But it also comes with one unavoidable responsibility, which is paying taxes.

If you are one of many small business owners who pay more tax than you think, and you think you are doing something wrong, you’re not. It is just because you are not yet knowledgeable enough for doing tax-saving strategies.

This time, you don’t need to worry about it. In this article, we will explain to you the best tax-saving strategies for small business owners who use an LLC. You’ll learn how to choose the right tax setup, claim deductions and credits, time your expenses wisely, and plan for 2026 and beyond.

How Does an LLC Help You Save on Taxes?

An LLC (Limited Liability Company) is one of the most flexible business structures for small business owners. It gives you limited liability protection — separating your personal assets from business debts — and tax flexibility that can lead to real savings.

By default, a single-member LLC is taxed as a sole proprietorship, while a multi-member LLC is taxed as a partnership. In both cases, profits “pass through” to the owners and are reported on their personal returns, avoiding corporate double taxation.

However, an LLC can also choose to be taxed as an S corporation or C corporation. These options don’t change your legal structure — only how the IRS taxes your income. That flexibility is what makes an LLC so useful for long-term tax planning.

How to Choose the Right Tax Structure for Your LLC

Your LLC’s tax structure determines how you report income, what taxes you pay, and which strategies you can use to save money.

Here’s a simplified comparison of your main options:

Tax Type | How It’s Taxed | Best For |

Sole Proprietorship (Default) | Income passes through to your personal tax return; you pay self-employment tax on all profits. | Single-member LLCs with modest income. |

Partnership (Default) | Profits are divided among members and taxed on each owner’s personal return. | Multi-member LLCs share profits. |

S Corporation (Elective) | Income is split between salary (subject to payroll tax) and distributions (not subject to self-employment tax). | Profitable LLCs (usually $60K+ in net profit). |

C Corporation (Elective) | The corporation pays its own taxes; dividends are taxed separately. | Larger LLCs are planning to reinvest profits or seek investors. |

Now, here’s how each option plays out in real life:

Sole Proprietorship: The simplest option. Easy setup and filing, but you’ll pay self-employment tax on your entire income.

Partnership: Great for flexibility and shared ownership, but partners still owe self-employment tax and must file Form 1065.

S Corporation: Offers major self-employment tax savings by splitting income between salary and distributions — but you must pay yourself a “reasonable” salary and handle payroll compliance.

C Corporation: Works best for businesses planning to scale or attract investors, but dividends face double taxation (corporate + personal).

Pro Tip:

If your business earns over roughly $60,000 per year, electing S-Corp status often strikes the best balance between simplicity and savings. To do this, file IRS Form 2553 within 75 days of forming your LLC or the start of a new tax year.

If you still need to review how your business structure affects your tax strategy, see our earlier piece about How to Choose the Right Business Structure: LLC vs. S-Corp Basics.

What Tax Deductions Can LLC Owners Claim in 2025?

Deductions reduce your taxable income, meaning less money owed to the IRS. LLC owners have access to a long list of legitimate deductions, many of which are underused.

Here are the major ones for 2025:

Deduction | What It Covers | 2025 Tip |

Qualified Business Income (QBI) | Deduct up to 20% of business profit | Review income limits; phaseouts may apply |

Section 179 Deduction | Equipment, computers, furniture, vehicles | Up to $1.22 million expensing limit |

Bonus Depreciation | Large asset purchases | 60% deduction in 2025 (phasing out) |

Home Office Deduction | Part of the home is used for business | Simplified: $5 per sq. ft., up to 300 sq. ft. |

Retirement Contributions | Solo 401(k), SEP IRA, SIMPLE IRA | Lowers taxable income and builds savings |

Health Insurance Premiums | Self-employed health plans | Deduct premiums for yourself and family |

Vehicle Expenses | Mileage or actual costs | Standard mileage rate applies |

Business Meals and Travel | 50% of qualified meals, travel, and lodging | Must be business-related and documented |

Startup Costs | Set up, legal, and initial expenses | Deduct up to $5,000 in the first year |

Tracking these consistently throughout the year makes tax season much easier and can even lead to more profit.

What Tax Credits Can Small Business Owners Use?

Unlike deductions, tax credits reduce your tax bill dollar-for-dollar. They can make a big difference for small business LLCs.

Some of the best credits available include:

R&D Credit: For developing new products or processes.

Work Opportunity Tax Credit (WOTC): For hiring workers from qualified groups.

Energy Efficiency Credits: For installing solar, EV chargers, or energy-efficient systems.

Paid Leave Credit: For offering paid sick or family leave (where applicable).

State-Level Credits: Many states offer small business hiring or investment incentives.

If your business is growing or hiring, talk to a CPA about which credits apply — many go unused each year.

How Can Timing Income and Expenses Reduce Taxes?

Timing is one of the simplest tax-saving strategies for small business owners. The idea is to control when you recognize income and when you pay expenses.

Examples:

Delay sending invoices until January to push income into the next year.

Prepay rent, insurance, or supplies before December 31 to claim the deduction early.

Make year-end retirement contributions.

If you expect a higher income next year, accelerate deductions now. If you expect lower income, consider deferring expenses. The goal is to smooth taxable income and stay within favorable brackets.

What Are Lesser-Known Tax Moves for LLC Owners?

Beyond the basics, a few smart tactics can add up to big savings:

Accountable Plans: Reimburse yourself for business expenses tax-free.

Hiring Family Members: Shift income into lower tax brackets.

Educational Expenses: Deduct training that improves your business skills.

Fringe Benefits: Offer health stipends or tuition assistance.

Section 1202 Exclusion: If converting to a C-Corp later, you may exclude capital gains on stock sales.

Each requires good documentation but can yield meaningful savings.

How to Handle State and Local Taxes as an LLC Owner

Federal taxes are only part of the picture. State and local rules can vary dramatically.

Key points:

Nexus: Having employees or property in multiple states may create tax obligations in each.

Pass-Through Entity (PTE) Taxes: Some states let LLCs pay state income tax directly to bypass the federal SALT cap.

Franchise or Gross Receipts Taxes: States like Texas or Washington impose these even without income tax.

Check your state’s small business tax guide annually — it’s easy to miss credits or deductions.

How to Keep Your Tax Deductions Audit-Proof

A good defense is the best tax strategy. The IRS audits small businesses more often than people think.

Stay safe by:

Keeping business and personal finances separate.

Saving receipts (digital is fine).

Using accounting software.

Keeping mileage logs and travel details.

Backing up records for at least three years.

If you can prove every deduction, you’ll have nothing to worry about.

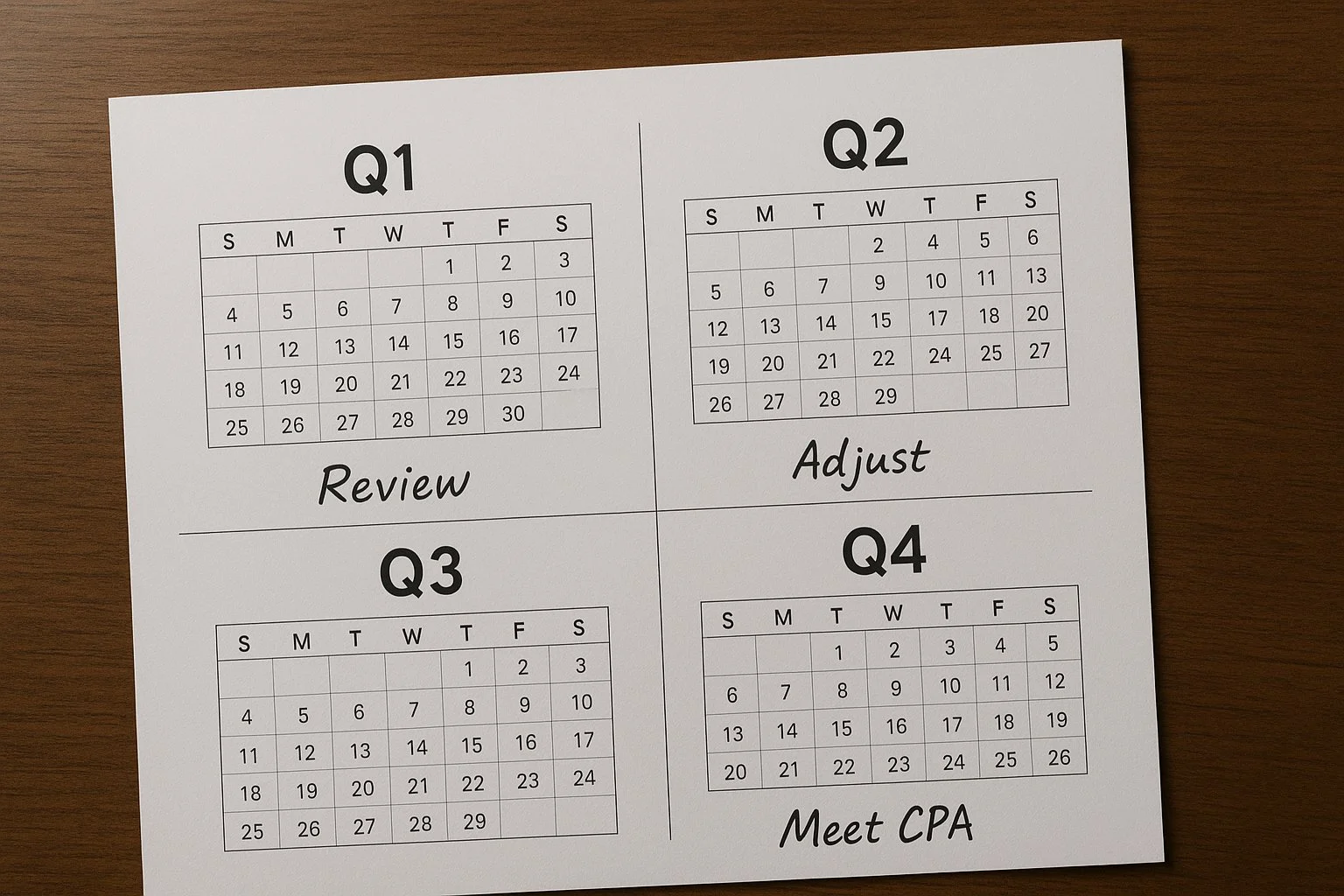

How to Plan Taxes Year-Round (Not Just in April)

The best way to save on taxes is to plan all year, not just when filing.

Here’s a simple routine:

Review your profit and expenses quarterly.

Adjust estimated tax payments as income changes.

Stay updated on new tax laws.

Meet with your accountant before year-end.

Planning early means more control and fewer surprises.

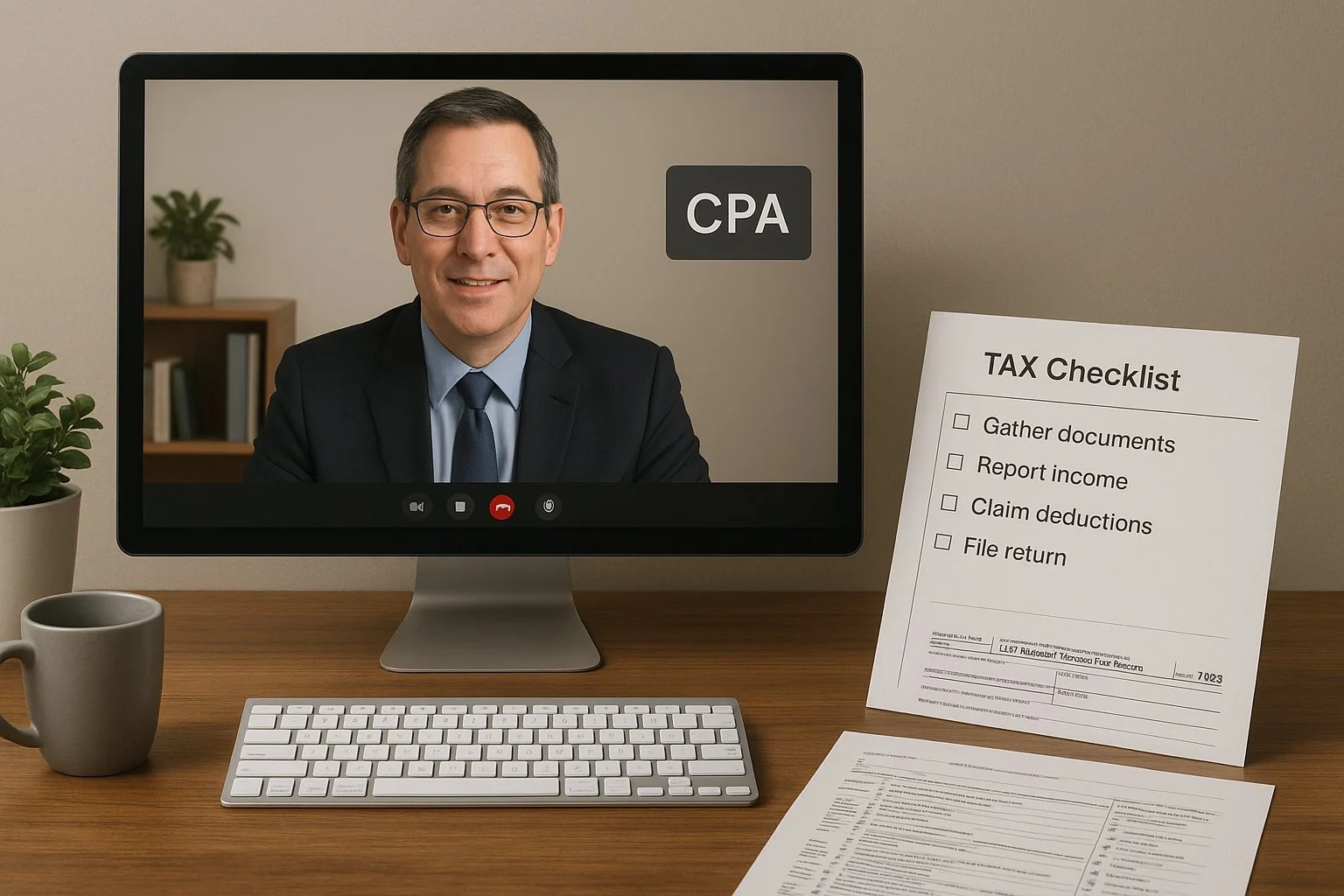

When Should an LLC Owner Hire a Tax Professional?

If your business is growing, it might be time to bring in expert help.

You’ve elected S-Corp status.

You have employees or multiple revenue streams.

You operate in more than one state.

You want proactive tax planning.

A good tax pro often saves more than they charge and keeps you compliant. But, keeping your LLC compliant isn’t just about taxes — it’s also about having the right legal foundation.

Learn why an Operating Agreement is essential for every LLC and how it helps prevent ownership disputes, protect liability status, and keep your business running smoothly.

What’s Coming Next for LLC Taxes After 2025?

Several provisions from the 2017 Tax Cuts and Jobs Act expire after 2025, including the QBI deduction and bonus depreciation. If Congress doesn’t extend them, small business taxes may rise.

Revisit your structure annually and plan — flexibility is your best advantage.

Conclusion

Taxes don’t have to drain your profits. With the right approach, structure, and timing, tax-saving strategies for small business owners can turn into long-term financial advantages.

Start by choosing the right classification for your LLC, tracking every expense, and planning ahead — not reacting after the fact. Even small adjustments, made early, can save thousands come tax season.

If you’re unsure which strategy fits best, talk with a qualified tax professional before year-end. A one-hour planning session now can easily pay for itself many times over.

Frequently Asked Questions

What are the different tax classification options available for an LLC?

An LLC can be taxed as a sole proprietorship (single-member), partnership (multi-member), S-corporation, or C-corporation. The default is pass-through taxation, but you can elect S-Corp or C-Corp status using IRS forms.

How does electing S-Corp status for my LLC help save on taxes?

Electing S-Corp status allows you to split income between salary and profit distributions. You pay payroll taxes on your salary only, which can significantly reduce self-employment tax while remaining compliant.

What common business expenses can I deduct as an LLC owner?

You can deduct operating expenses like rent, supplies, insurance, marketing, business travel, meals (50%), equipment, home office use, and retirement plan contributions. Always keep receipts and proof of business purpose.

What is the best way for an LLC to file taxes?

The best way for an LLC to file taxes depends on how it’s structured. A single-member LLC files through Schedule C with their personal return. Multi-member LLCs file Form 1065 and issue K-1s. Many LLCs also elect S-Corp status to reduce self-employment tax.

Are there any tax credits available specifically for small business LLC owners?

Yes. Common ones include the R&D Credit, Work Opportunity Tax Credit, and energy-efficiency incentives. Many states also offer small business hiring or investment credits.

Can an LLC owner avoid self-employment tax?

Partially. S-Corp owners can reduce self-employment tax by paying a reasonable salary and taking the remaining profit as distributions.

Are LLC startup costs deductible?

Yes. You can deduct up to $5,000 in startup costs and $5,000 in organizational expenses in your first year.

How do you pay yourself from an LLC?

Single-member LLCs take owner’s draws. S-corps must pay a salary (through payroll) and can take distributions on top of that.

What’s the best way to lower quarterly taxes?

Make estimated payments based on real income, track deductions monthly, and adjust contributions like retirement or health insurance before deadlines.

Do LLC owners qualify for the 20% QBI deduction?

Yes. Most small LLC owners qualify for up to 20% off business income, though high earners may face limits based on income and business type.