QBI Deduction Explained: Eligibility and Tips for Small Business Owners

Gary Gal

Taxes can feel like a maze, especially when you run your own business. One of the most valuable tax breaks for small business owners right now is the Qualified Business Income (QBI) deduction, also known as the Section 199A deduction.

This deduction lets many business owners deduct up to 20% of their qualified business income from their taxable income. It’s a simple concept that can lead to big savings. Whether you’re a solo freelancer, a small business owner, or managing an LLC, understanding how the QBI deduction works can help you keep more of your earnings.

Let’s break down how it works, who qualifies, how to calculate it, and the best ways to maximize your deduction before it potentially expires after 2026.

What Is the QBI Deduction and Why Does It Matter

The Qualified Business Income deduction was created under the Tax Cuts and Jobs Act (TCJA) of 2017 to give small business owners a tax break similar to what corporations received. It allows eligible taxpayers to deduct up to 20% of qualified business income (QBI) from pass-through entities.

If you run a sole proprietorship, partnership, S corporation, or certain LLC, your business income “passes through” to your personal tax return. The QBI deduction helps you lower your taxable income by recognizing that you are both the owner and the worker in your business.

This deduction doesn’t require you to spend money or buy anything—it’s simply a reward for generating business income. It’s available through tax year 2025, unless extended by Congress.

How the QBI Deduction Works (The 20% Rule)

The QBI deduction is based on a straightforward formula: you can deduct 20% of your qualified business income from your taxable income.

Here’s the breakdown:

QBI Portion: Up to 20% of your qualified business income.

Investment Portion: Up to 20% of qualified REIT dividends and Publicly Traded Partnership (PTP) income.

It’s claimed on your personal tax return (Form 1040), not on your business tax return. You can take it whether you itemize deductions or take the standard deduction.

However, it doesn’t reduce your self-employment tax—only your taxable income.

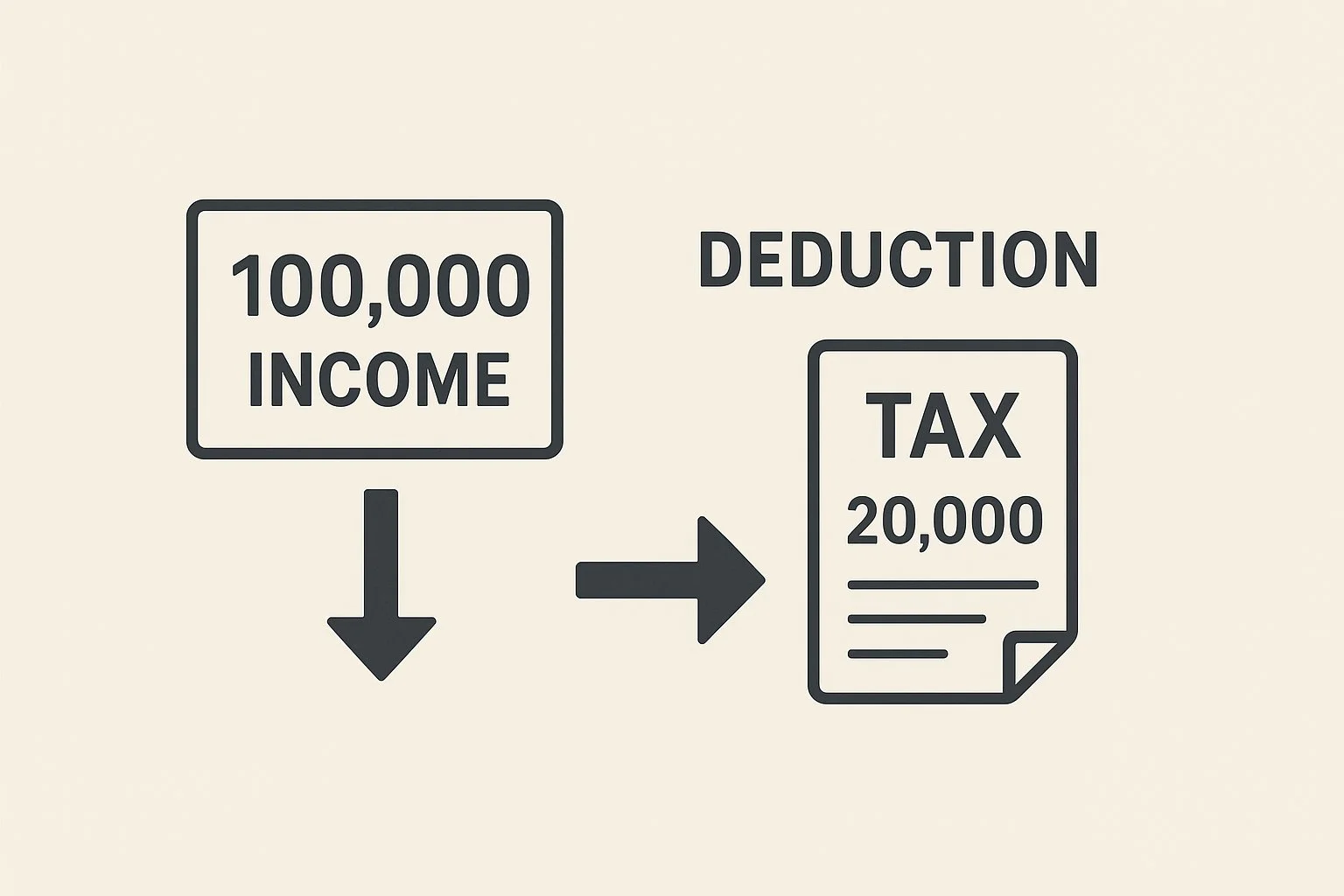

Example:

If your small business earns $100,000 in qualified business income, you may be able to deduct $20,000, which could significantly lower your tax bill.

Who Qualifies for the QBI Deduction

The QBI deduction is available only to owners of pass-through entities—businesses that don’t pay corporate tax but instead pass profits through to the owner’s personal return.

Eligible Entities

Sole Proprietorships

Partnerships

LLCs (taxed as a sole proprietorship or partnership)

S Corporations

Certain trusts and estates

Not Eligible

C Corporations

Employees who earn W-2 wages

What Counts as Qualified Business Income

Qualified Business Income generally means your net profit from business operations in the U.S., minus ordinary deductions.

Income that does not qualify:

Capital gains and losses

Dividends or interest (not related to business activity)

Foreign income

Guaranteed payments to partners

If your business earns from regular operations—selling products, providing services, or renting qualifying real estate—your income likely counts as QBI.

QBI Deduction Income Limits (2026 Update)

The IRS limits the QBI deduction based on taxable income, which changes each year due to inflation.

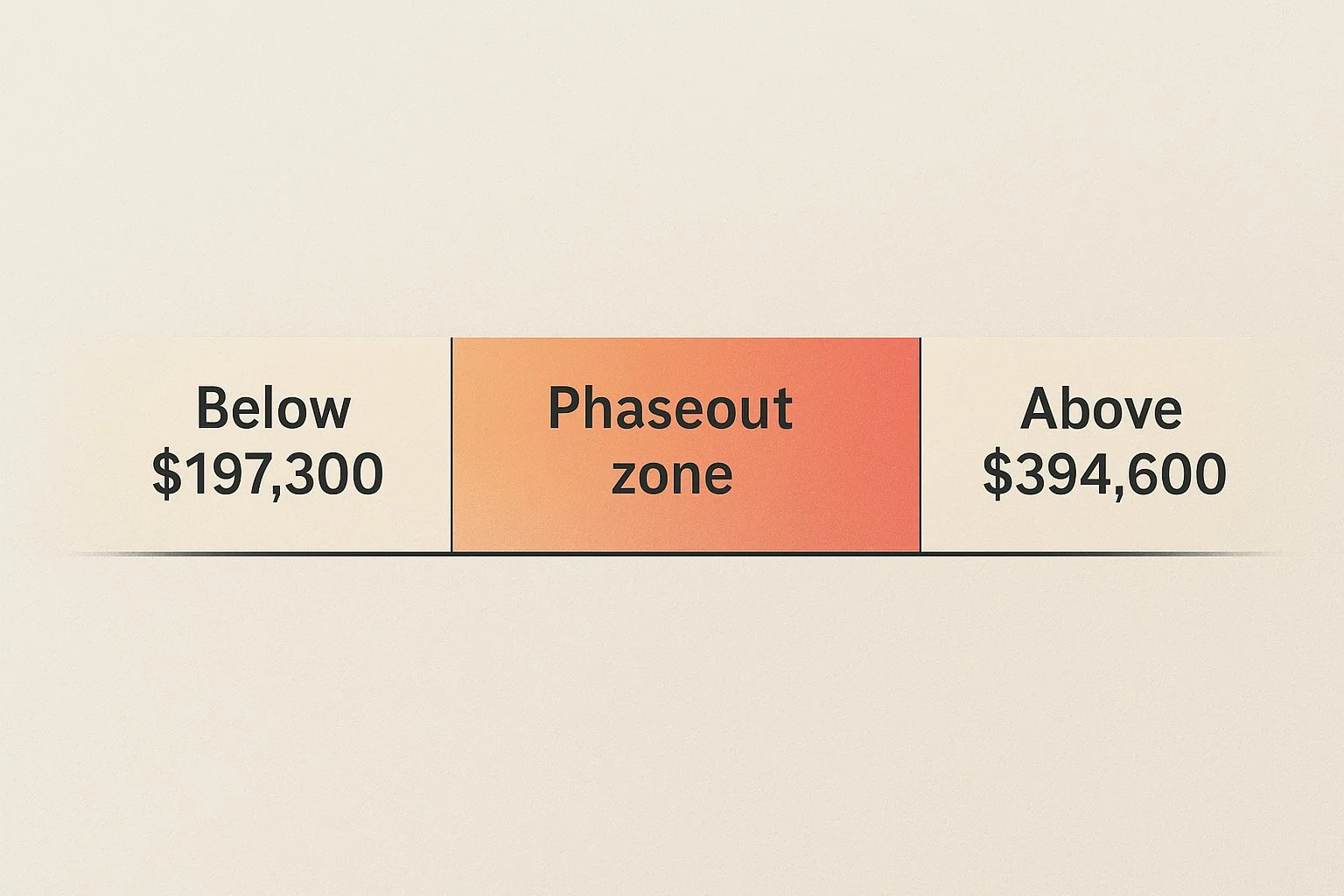

For 2025, the thresholds are:

Single filers: $197,300

Married filing jointly: $394,600

Here’s how the limits work:

Below the threshold: You can claim the full 20% deduction, no matter the business type.

Within the phase-in range: The deduction starts to shrink, depending on W-2 wages paid and the Unadjusted Basis Immediately After Acquisition (UBIA) of qualified property.

Above the upper limit: The deduction becomes limited or may disappear entirely for certain service-based businesses.

If you own a non-service business, you may still claim a partial deduction based on W-2 wages and property values.

How to Calculate the QBI Deduction (Step-by-Step Example)

Let’s go through the basic steps to calculate your deduction.

Step 1: Find Your Qualified Business Income

Start with your business’s net income, subtract business expenses, and exclude non-qualified income like capital gains.

Step 2: Multiply by 20%

Multiply your QBI by 20%.

Example: $100,000 × 20% = $20,000.

Step 3: Apply Income Thresholds

If your taxable income is below the threshold, you can take the full $20,000 deduction.

If it’s higher, use the wage and property limits to see how much of that deduction you can actually keep.

Step 4: Apply the Overall Cap

The total QBI deduction can’t exceed 20% of your taxable income minus capital gains.

Taxable Income | Qualified Business Income | 20% of QBI | Allowed Deduction |

$80,000 | $80,000 | $16,000 | $16,000 |

$200,000 | $200,000 | $40,000 | $40,000 |

$420,000 (joint) | $420,000 | $84,000 | Phaseout applies |

Special Situations by Business Type

Every business structure interacts with the QBI deduction a little differently.

LLCs and Sole Proprietors

You report income on Schedule C, and the QBI deduction flows through to your personal tax return. Simple and direct.

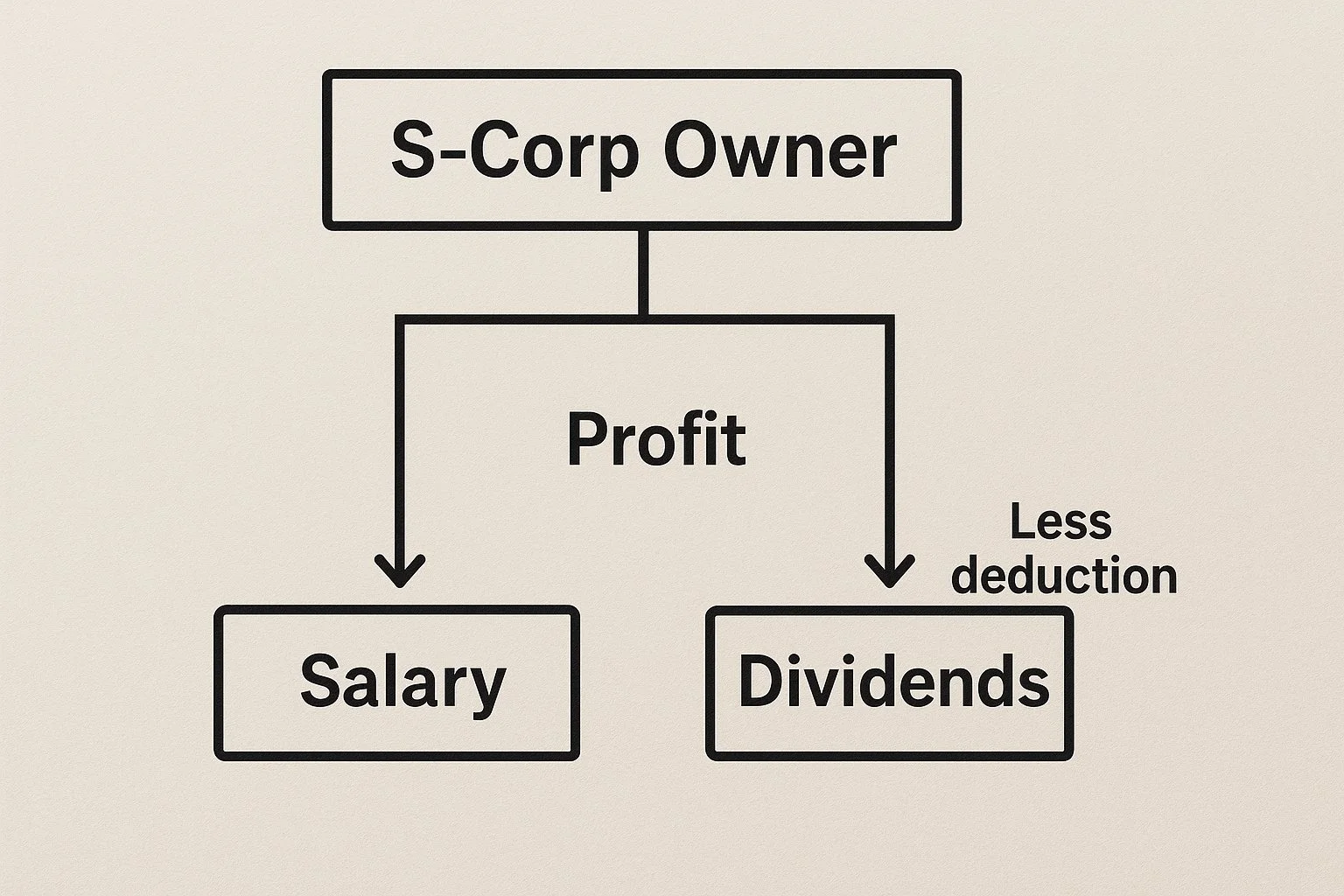

S Corporations

S-Corp owners must pay themselves a reasonable salary. The QBI deduction applies only to profits, not wages, so setting the right mix of salary and distribution matters.

Partnerships

Each partner claims their own share of the QBI deduction on their individual return, based on their percentage of ownership.

Rental Real Estate

Rental income can qualify if it meets the IRS safe-harbor rule. That generally means:

Separate books for rental activity

At least 250 hours of rental services per year

Documented records of maintenance and management activity

For a deeper look at when an LLC should elect S-Corp status, check out Should my LLC be taxed as an S-Corp?

Tax Planning Tips to Maximize Your QBI Deduction

Here’s how small business owners can make the most of the QBI deduction:

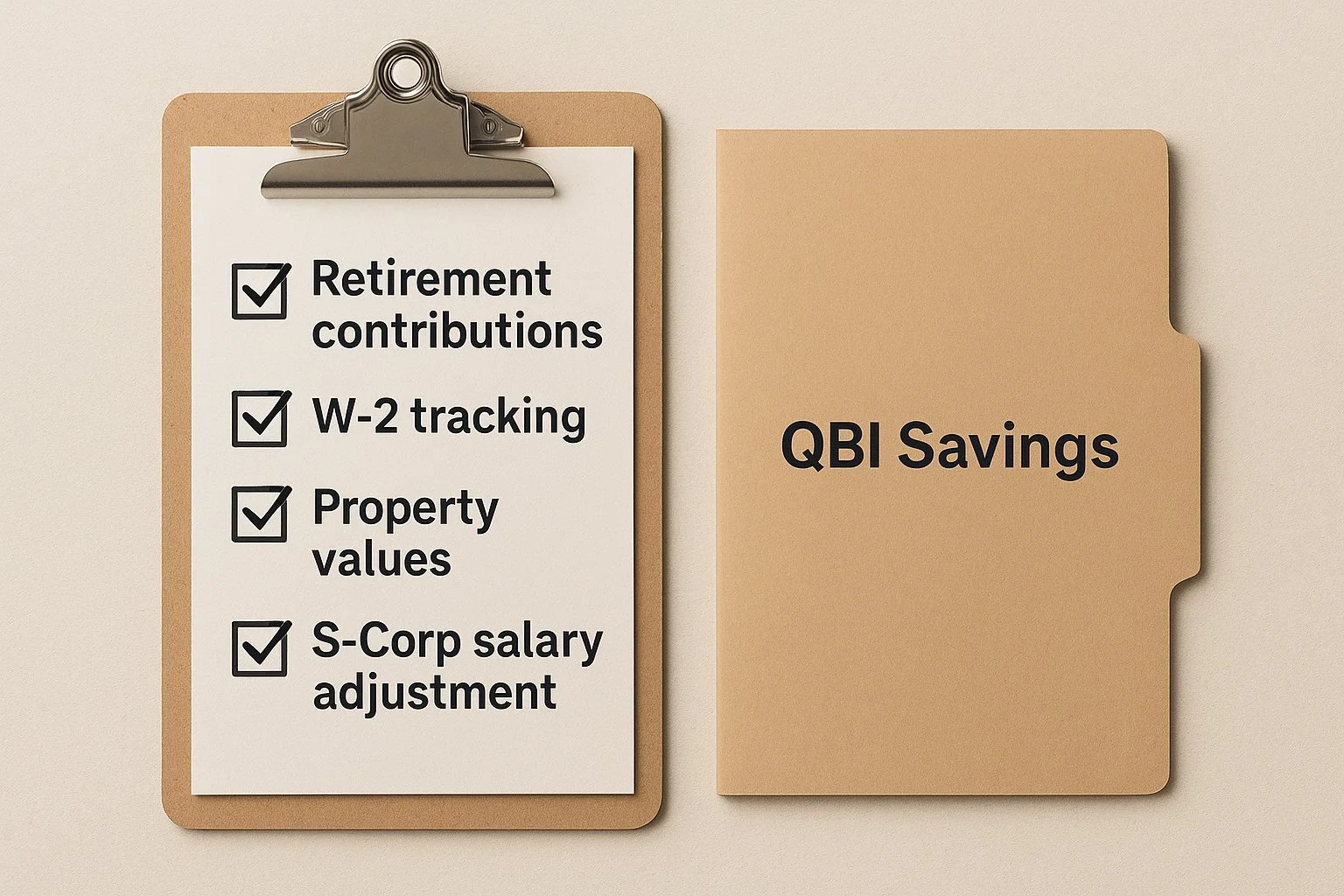

Track wages and property values.

W-2 wages and the UBIA of business property determine how much deduction you can take above the income threshold.Keep taxable income below the limit.

Use retirement contributions (401(k), SEP IRA) or health savings accounts (HSAs) to stay below the threshold.Aggregate related businesses.

The IRS lets you combine businesses with shared ownership, which can help you qualify under wage or property rules.Review your S-Corp salary.

A lower salary with higher profit can increase your deduction—but be sure it’s “reasonable” under IRS guidelines.Work with a tax professional.

QBI rules are detailed. A professional can help ensure your structure and deductions align for the biggest benefit.

You can also explore more tax-saving strategies for small business owners with an LLC to find additional ways to reduce taxable income and stay under the QBI thresholds.

Common Mistakes to Avoid

A few common errors can cause small business owners to miss out or trigger IRS issues:

Including non-qualified income like capital gains or dividends.

Skipping documentation for wages, property basis, or business records.

Overlooking income phaseouts. Once you pass limits, the formula changes.

Assuming every business qualifies. Some service businesses face restrictions.

Ignoring the expiration date. The QBI deduction may end after 2025 unless extended.

Setting up solid internal agreements helps, too. Here’s why every LLC needs an operating agreement to stay compliant and organized for tax season.

Final Thoughts and Resources

The QBI deduction is one of the most powerful tools for small business tax savings. It rewards entrepreneurs, freelancers, and small business owners by cutting taxable income—often saving thousands each year.

Because the deduction may expire after 2025, it’s important to plan. Keep detailed records, manage your taxable income, and talk with a tax professional to ensure you qualify for the maximum benefit.

Helpful Resources

IRS Form 8995 & 8995-A: For calculating and reporting your deduction

IRS QBI Overview: Official IRS Page on Section 199A

Tax Software Tools: Many include a built-in QBI deduction calculator

SSTB Guide: For detailed income limits and service business rules

Frequently Asked Questions

What is the QBI deduction?

The Qualified Business Income deduction lets eligible business owners deduct up to 20% of their qualified business income, helping reduce overall taxes. It applies to most pass-through businesses.

Who qualifies for the QBI deduction?

Sole proprietors, partners, S corporation shareholders, and certain trusts or estates qualify. C corporations and employees do not.

How do I calculate my QBI deduction?

Take 20% of your qualified business income and compare it to 20% of taxable income (minus capital gains). The smaller number is your deduction.

Is rental income eligible for the QBI deduction?

Yes, if the rental activity meets the IRS safe-harbor rules for a trade or business.

Does an LLC qualify for the QBI deduction?

Yes, if the LLC is taxed as a pass-through entity and earns qualified business income.

What are the 2025 QBI income limits?

Single filers: $197,300. Married filing jointly: $394,600. Deduction phases out beyond those amounts.

Can I claim the QBI deduction if I’m self-employed?

Yes. Self-employed individuals can claim it on the income reported on Schedule C.

What businesses are excluded from QBI?

C corporations, employee wages, and income from investments or foreign sources.

How do phaseouts work for high earners?

Above income limits, deductions depend on W-2 wages and business property values. Some high-earning service businesses lose eligibility.

Will the QBI deduction expire after 2025?

Yes, unless Congress extends it. It’s currently set to end after the 2025 tax year.