Should My LLC Be Taxed as an S-Corp? A Step-by-Step Decision Checklist

Gary Gal

When you start an LLC, one of the major financial decisions you’ll face is how it should be taxed. By default, an LLC’s income passes through to the owner’s personal return, and all profits are subject to self-employment taxes. But there’s another option: electing to have your LLC taxed as an S-Corporation (S-Corp).

On paper, that change might sound small. In practice, it can impact how much you pay in taxes, how you pay yourself, and how much time you spend managing paperwork. This guide walks you through each step to help you decide if an S-Corp election makes sense for your LLC.

Step 1: Clarify What Changes with S-Corp Taxation

An LLC taxed as an S-Corp keeps the same legal protection and structure, but it’s still an LLC. The difference is purely tax-related. Normally, an LLC’s profits are treated as self-employment income, and owners pay roughly 15.3% in self-employment taxes on all net profits.

When taxed as an S-Corp, the IRS lets you divide income into two parts:

A salary (taxed with FICA payroll taxes)

Distributions (not subject to self-employment taxes)

This distinction can lead to tax savings because only the salary portion is subject to Social Security and Medicare taxes. The rest of your profit is taxed at regular income tax rates.

However, the IRS requires that the salary you pay yourself be “reasonable” — meaning it reflects the market rate for the work you actually perform.

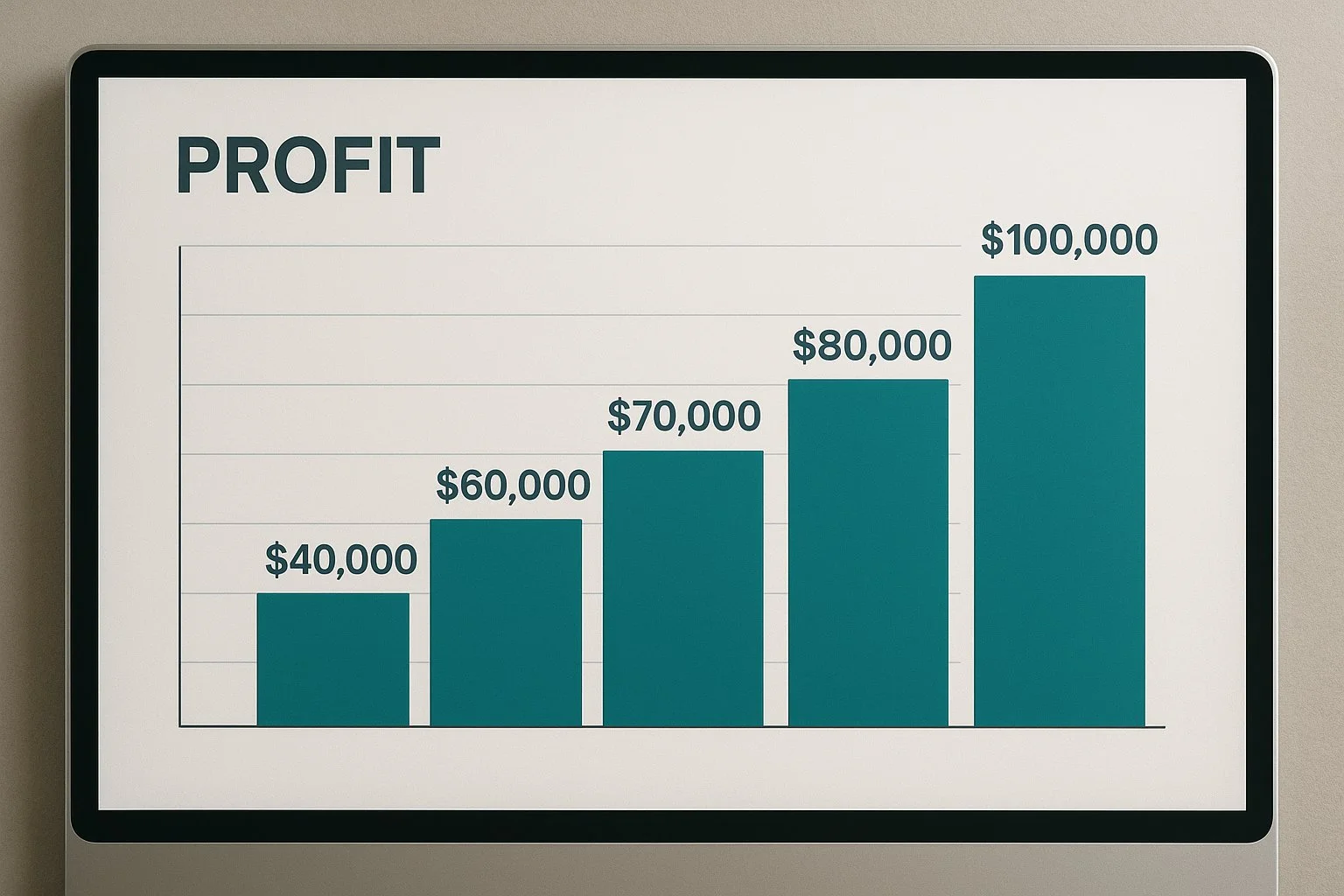

Step 2: Evaluate Your Income and Profit Consistency

S-Corp status tends to benefit business owners once their net profit (after expenses) reaches about $60,000 to $100,000 per year consistently. At that point, splitting income between salary and distributions can reduce your self-employment tax burden.

For example, if your LLC earns $100,000:

As a standard LLC, you’d pay self-employment tax on all $100,000.

As an S-Corp, if you paid yourself a $50,000 salary and took $50,000 as distributions, only the salary would be hit with FICA taxes.

That alone could save you around $7,000–$8,000 annually in self-employment taxes.

Still, the math only works if profits are steady and the extra administrative work doesn’t cancel out the savings.

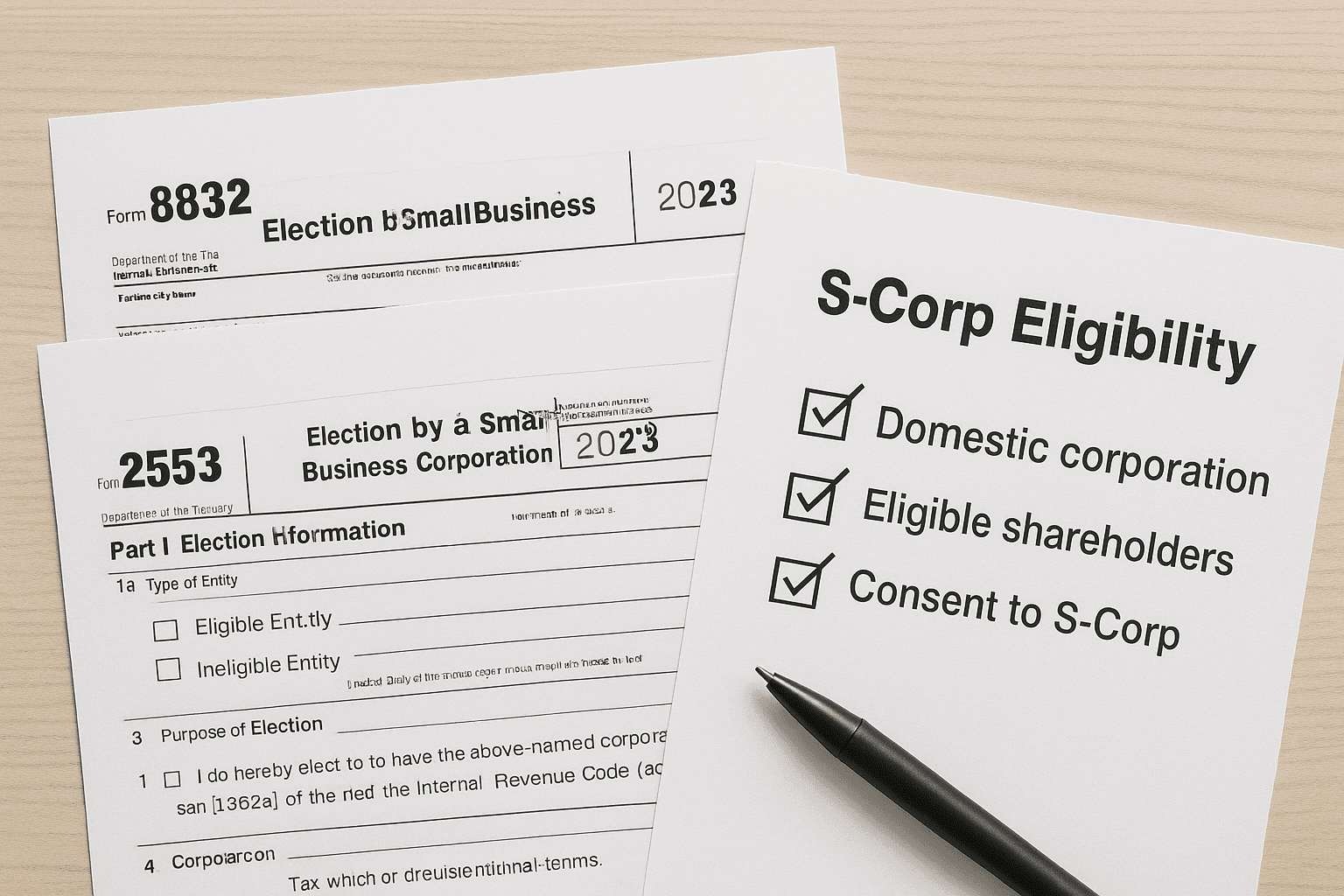

Step 3: Check IRS Eligibility and Filing Requirements

Before you can switch, your LLC must meet the IRS’s S-Corp eligibility criteria:

It must be a domestic entity.

It can have no more than 100 shareholders (owners).

All shareholders must be U.S. citizens or residents.

You can have only one class of ownership interest (no preferred shares).

If your LLC is currently taxed as a sole proprietorship or partnership, you’ll first file Form 8832 to elect corporate taxation. Then, you’ll submit Form 2553 (Election by a Small Business Corporation) to officially elect S-Corp status.

Timing matters. You have 2 months and 15 days from the start of the tax year to file Form 2553 if you want the change to apply that year.

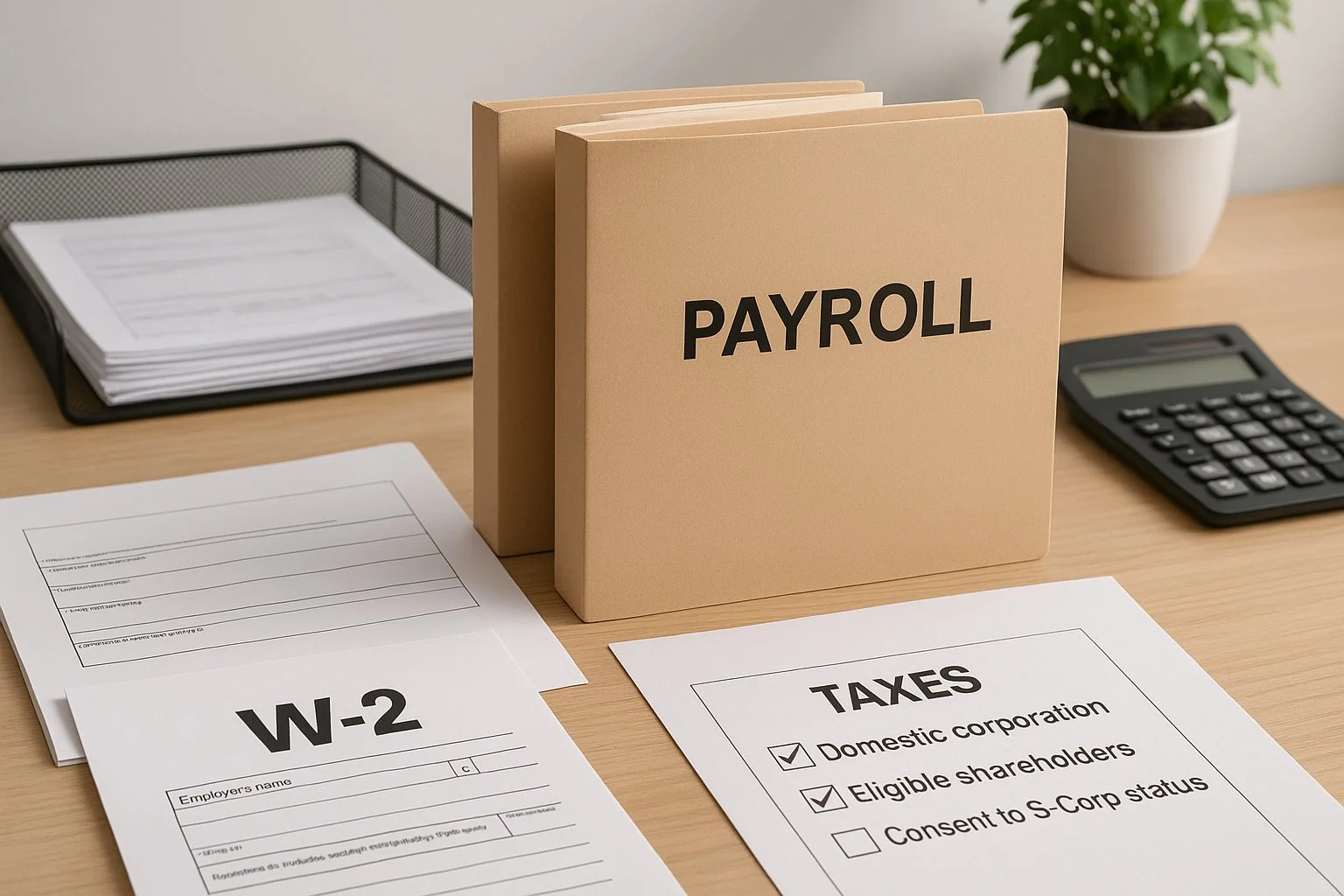

Step 4: Consider Payroll and Administrative Impact

Once your LLC becomes an S-Corp, you’ll essentially be both the owner and an employee. That means:

You must run payroll for yourself and any other working owners.

You’ll need to withhold payroll taxes, issue W-2s, and file quarterly payroll tax returns.

You’ll file a corporate return (Form 1120-S) each year, and issue K-1 forms to owners for reporting their share of profits.

These new requirements often mean hiring a payroll provider or accountant, which adds costs. For many business owners, these fees are small compared to the tax savings—but they still matter.

If your business is small or just getting started, the added paperwork can outweigh the benefit.

Step 5: Identify the Financial Trade-Offs

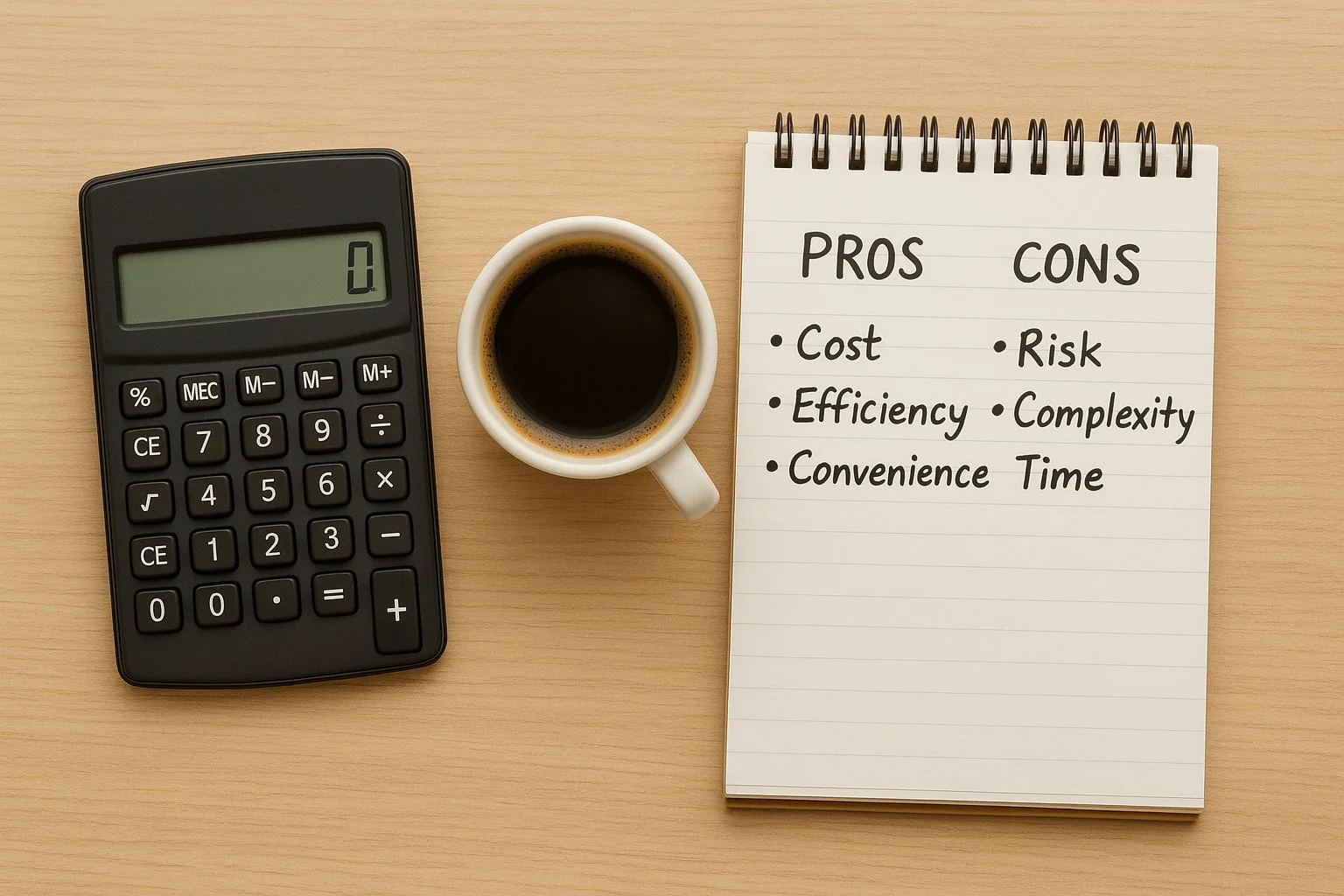

Pros of Electing S-Corp Status

Lower self-employment taxes on profits above a reasonable salary.

Potential 20% Qualified Business Income (QBI) deduction, available through 2026 under current tax law.

Greater flexibility in how owners receive income (salary vs. distributions).

Possible perception boost for business credibility with clients and lenders.

Cons of Electing S-Corp Status

More complex recordkeeping and tax filings.

Need to determine and justify reasonable compensation.

Additional payroll service costs and possibly state-level franchise taxes.

Not ideal for LLCs with low or inconsistent profits.

Bottom line: S-Corp status is financially rewarding only if your profits are high enough to offset the cost of compliance.

Step 6: Run a Simple Pro Forma Comparison

Before filing anything with the IRS, run a side-by-side comparison:

Estimate your net profit for the year.

Decide what would be a reasonable salary for your role.

Calculate payroll taxes on that salary.

Add estimated payroll service and accounting fees.

Compare your total tax burden as a regular LLC versus an S-Corp.

For example:

Scenario | LLC Default | S-Corp |

Net Income | $100,000 | $100,000 |

Salary | N/A | $50,000 |

Payroll Taxes (FICA) | $15,300 | $7,650 |

Admin Costs | $0 | $2,000 |

Total Tax & Costs | $15,300 | $9,650 |

In this scenario, the S-Corp setup saves about $5,650—worth it if your profits stay consistent.

Step 7: Make and Maintain the Election

Once you’ve decided, here’s how to make it official:

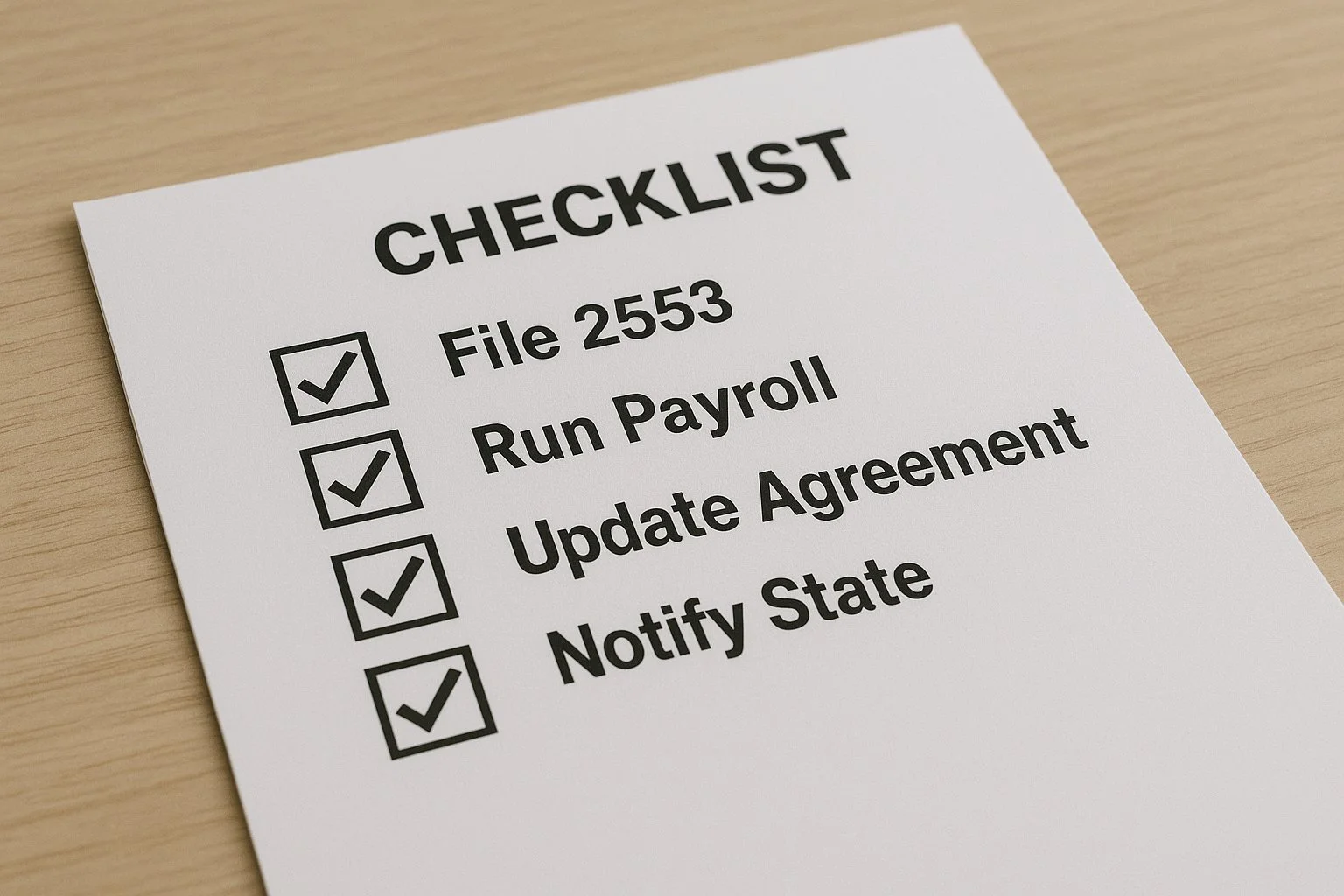

File Form 2553 with the IRS within 2 months and 15 days of the tax year start.

Set up payroll for yourself and any co-owners.

Update your LLC’s operating agreement to reflect new governance and compensation rules.

Notify your state if it requires separate S-Corp recognition (some states do).

Maintain compliance: run payroll correctly, file quarterly taxes, and keep meeting minutes.

If you miss deadlines or don’t follow the rules, the IRS can revoke your S-Corp status — so consistency matters.

Step 8: Reevaluate Periodically

Electing S-Corp status isn’t a one-time decision you should forget about. Your income, expenses, or even tax laws can shift over time.

If profits drop, you may find that the savings disappear once you factor in accounting and payroll costs. Conversely, as your business grows, S-Corp treatment might become even more beneficial.

It’s smart to revisit your setup annually with your CPA to confirm it’s still the right fit.

Conclusion: The Smart Way to Decide

An S-Corp election can be a smart financial move for profitable LLCs, but it’s not a shortcut for everyone. You’ll likely benefit if:

Your LLC earns steady profits of over $60,000 annually.

You’re ready to handle or outsource payroll.

You want to legally minimize self-employment taxes.

If you’re unsure, run the numbers or talk with a small business tax professional. The best choice depends on your profit margins, growth plans, and how much administrative work you’re comfortable managing.

Tip: Treat this as a tax strategy, not a status symbol. The right answer is the one that leaves more money in your pocket after taxes and compliance costs.

Once you’ve completed the checklist and decided on your tax classification, revisit our full structure-choice guide to review ownership, liability, and growth implications.

Frequently Asked Questions

What’s the main difference between an LLC and an S-Corp for taxes?

An LLC pays self-employment taxes on all profits. An S-Corp allows owners to split income between salary and distributions, reducing self-employment tax liability.

Can any LLC elect to be taxed as an S-Corp?

Most can, but you must meet IRS eligibility rules: be a domestic entity, have 100 or fewer shareholders, one class of stock, and all owners must be U.S. citizens or residents.

How do I file for S-Corp taxation?

Submit Form 2553 to the IRS. If your LLC was previously taxed as a partnership or sole proprietorship, file Form 8832 first.

When should I file Form 2553?

You must file within 2 months and 15 days of the start of the tax year you want the election to apply.

What counts as a “reasonable salary” for S-Corp owners?

It’s the amount you’d pay someone else to perform your same role. The IRS considers factors like job duties, industry standards, and experience.

Do I still pay self-employment tax as an S-Corp owner?

You’ll pay payroll (FICA) taxes on your salary, but not on distributions. This is where potential savings come from.

What are the ongoing costs of running an S-Corp?

Expect payroll service fees, bookkeeping, tax filing costs, and possibly state franchise or S-Corp taxes.

Can I switch back to regular LLC taxation later?

Yes, but it requires filing paperwork and may have timing restrictions. A CPA can guide you through reverting.

Does my state recognize S-Corp elections?

Not all states do. Some treat S-Corps the same as regular corporations for state tax purposes, while others honor the federal election.

What if my LLC doesn’t make a consistent profit?

If your income fluctuates or is low, the extra costs of payroll and compliance might outweigh any tax savings. In that case, staying with default LLC taxation may be smarter.